Teaching in Minnesota has become more demanding in recent years. Expectations are higher, classrooms are more complex, and many veteran educators are reassessing their retirement timelines.

Under the rules of the Minnesota Teachers Retirement Association, or TRA, early retirement is possible. But it is not neutral. Retiring before full retirement age may trigger a permanent actuarial reduction to your monthly pension benefit.

The real question is not whether you can retire early. It is how much it will cost over the course of your lifetime.

This guide explains the Minnesota TRA early retirement reduction formula, shows how the reduction is calculated, and walks through real examples so you can evaluate the decision with precision.

What Is the Minnesota TRA Early Retirement Reduction?

Under the rules of the Minnesota TRA, teachers may begin collecting retirement benefits before reaching full retirement age. However, starting benefits early permanently reduces the monthly amount.

This reduction is actuarial. It is not a temporary penalty, and it does not disappear once you reach full retirement age. The benefit is adjusted because it is expected to be paid over a longer period of time.

The reduction percentage is determined by your age at retirement relative to your tier’s full retirement age. The younger you are when benefits begin, the larger the permanent reduction.

The key variables are:

• Your tier status, Tier I or Tier II

• Your full retirement age

• Your age when benefits begin

To determine your Tier status, check out our full guide.

If you are unsure which tier applies to you, clarify that first. Tier status determines your full retirement age and the applicable reduction schedule.

Where to Find the Official TRA Reduction Factors

TRA publishes early retirement reduction factors organized by age at retirement. For each year below full retirement age, a specific actuarial reduction percentage applies.

The schedule is structured around:

• Your tier

• Your full retirement age

• Your age when you begin collecting benefits

The reduction is permanent. Beginning benefits at age 62 instead of full retirement age will lock in the reduced amount for life.

Always verify your specific reduction factor using official TRA materials before making a decision.

How the Reduction Is Applied

The reduction is applied after your base pension benefit is calculated.

Step 1: Calculate Your Base Pension Benefit

Your base benefit is determined by:

• Your High-5 average salary

• Years of allowable service

• The TRA accrual formula

To determine how to calculate your base benefit, see our Pension Calculation post.

If you do not understand your base benefit, the reduction percentage will not be meaningful.

Step 2: Identify Your Full Retirement Age

Full retirement age differs by tier.

Tier I and Tier II members both have a normal retirement age of 65. However, Tier I members may qualify for an unreduced benefit under the Rule of 90, while Tier II members do not.

The reduction schedule measures your retirement age against this benchmark.

Early retirement reductions apply when benefits begin before normal retirement age.

Step 3: Apply the Age-Based Reduction Factor

Once you determine your age at retirement, you locate the corresponding reduction percentage.

For example:

• Retiring three years before full retirement age results in a specific actuarial reduction.

• Retiring ten years before full retirement age results in a much larger reduction.

The younger you are at retirement, the larger the permanent adjustment.

Real Minnesota Scenarios

These examples assume current TRA reduction factors and a full retirement age of 65.

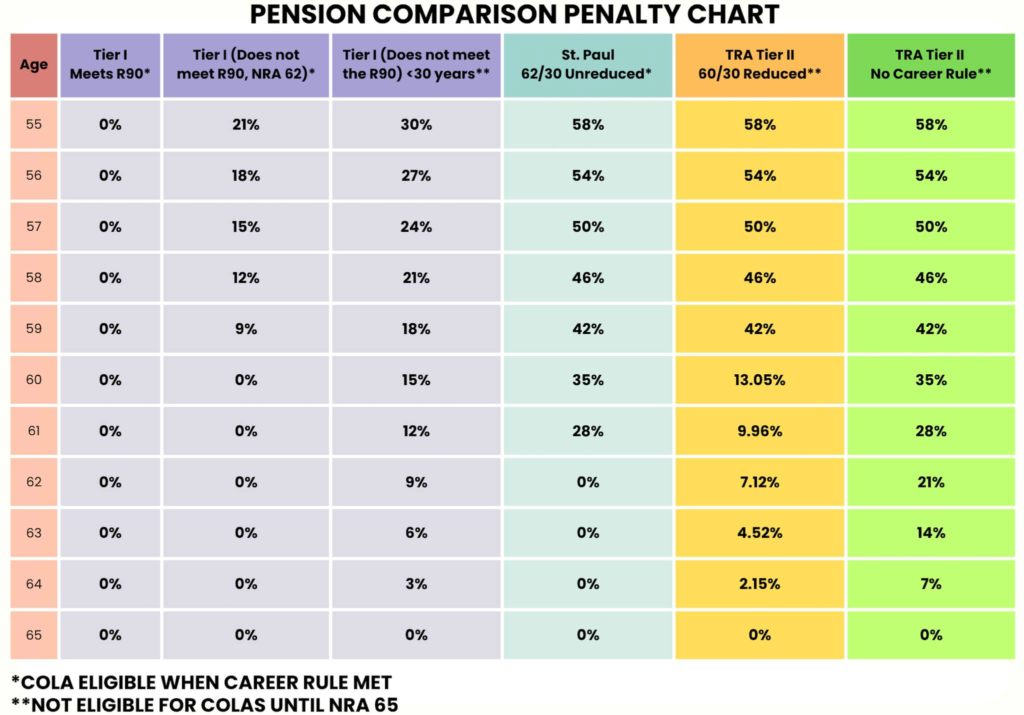

Example 1: Tier I Teacher Retiring at Age 60

Assume:

• 25 years of service

• A calculated base pension of $3,000 per month at full retirement age

Since full retirement age is 65 and the teacher retires at 60, the TRA age-based reduction factor applies. Because this person did not fulfill the Rule of 90, their reduction would be 15%. A Tier I teacher retiring at age 60 with 30 years of service would meet the Rule of 90 and receive an unreduced benefit

This means that their $3,000 benefit now becomes $2,550. That $450 less per month becomes $5,400 per year. Over a 25 year retirement that is $135,000 in lost income.

Example 2: Tier II Teacher Retiring at 62

Tier II members typically face larger reductions when retiring before full retirement age.

Assume:

• A calculated base benefit of $3,200 per month

• Retirement at age 62 with 25 years of service

• Full retirement age at 65

This member would face a 21% reduction.

That is a $672 monthly permanent reduction.

Over decades of retirement, that difference compounds significantly.

Check out our post on the key early retirement provision for Tier II: The “60-30 enhanced” rule.

Example 3: Retiring at 55

Retirement at 55 may be permitted depending on service requirements, but the reduction percentage at that age can exceed 50% depending on your tier!

For many teachers, retiring at 55 without significant supplemental savings can drastically reduce long-term retirement income.

For help planning your future retirement under this scenario, check out our Teacher Finance 101 guide.

For this type of early retirement, you’ll also want to check out our 403b guide.

This is where planning outside the pension system becomes essential.

Tier I vs Tier II Differences in Early Retirement

Tier I members generally have:

• Lower penalties

• More favorable early retirement treatment

Tier II members:

• Higher full retirement ages

• Larger age-based reductions when retiring early

Before making a decision, confirm your tier and your exact full retirement age. Those two variables determine your reduction factor.

When Early Retirement May Be Reasonable

Early retirement is not automatically a mistake.

It may make sense if:

• You have built substantial 403b or Roth IRA assets

• You plan to continue working part-time

• Health or family priorities outweigh maximizing pension income

• You separate from employment but delay beginning benefits

The sequence should be:

- Calculate the base pension.

- Apply the age-based reduction factor.

- Measure the permanent income difference.

- Evaluate whether other assets can close the gap.

Retirement timing should be based on mathematics first. Emotion can inform the decision, but it should not override the math.

Common Misunderstandings

• The reduction does not disappear when you reach full retirement age.

• It is not a temporary penalty.

• Working elsewhere does not restore the unreduced benefit.

• The Rule of 90 determines eligibility for Tier I members. It does not eliminate age-based reductions unless the Rule of 90 threshold is met.

Check out our Rule of 90 guide for more information.

Eligibility and actuarial reduction are separate concepts.

Bottom Line

The Minnesota TRA early retirement reduction schedule exists to quantify the cost of beginning benefits before full retirement age.

Retiring early is allowed. It is not neutral.

The difference between retiring at full retirement age and retiring several years early can represent hundreds of dollars per month and potentially six figures over a lifetime.

Before making the decision, confirm:

• Your tier

• Your full retirement age

• Your calculated base benefit

• The official age-based reduction percentage

Once those numbers are clear, you can decide whether early retirement aligns with your broader financial plan.

Frequently Asked Questions About Minnesota TRA Early Retirement

Can Minnesota teachers retire at age 55?

Yes, depending on tier and years of service. However, retiring at age 55 typically results in a significant age-based reduction unless a Tier I member qualifies under the Rule of 90. The reduction at age 55 can exceed 50 percent depending on tier.

Does the Rule of 90 eliminate early retirement reductions?

For Tier I members who meet the Rule of 90 threshold, the pension is unreduced. If the Rule of 90 is not met, the age-based reduction schedule applies. Tier II members are not eligible for the Rule of 90.

Is the Minnesota TRA early retirement reduction permanent?

Yes. The reduction is permanent and does not increase once you reach full retirement age. The benefit amount is locked in at the age payments begin.

How much does TRA reduce benefits at age 62?

The reduction percentage depends on your tier and full retirement age. The official TRA reduction schedule lists the actuarial percentage for each retirement age below full retirement age. Always verify your specific factor using current TRA materials.

Leave a Reply

You must be logged in to post a comment.