Now it the time to have those conversations about money with the ones that you love.

A year ago, one of our firsts posts was discussing the importance of having money conversations with your family. It is challenging to have those financial conversations with the people around you. Often people can be ashamed and consider it a blow to their ego when comparing bank accounts. But now, a time of uncertainty is the perfect time to have these conversations. Some tips to start these conversations on the right foot.

1. Talk proactively – No one can control the previous money mistakes that we have made. We have all made several. I make financial mistakes almost weekly, and that’s okay. Don’t dwell on the past but instead frame your conversation as it applies to the future. Saying things like, “What bills and debts do we needs to pay down this month?”, “How much do you think we could afford to invest?” “How much do you think we should budget for groceries next month?” All of those kinds of questions avoid looking at past financial mistakes and focus on future expenses or investments.

2. Don’t compare bank accounts – Net worth is a very nice stat for individuals to track to monitor overall financial well-being. But what might be a good spot for you won’t necessarily be a good spot for someone else. Directly comparing salaries, bank accounts, investments, etc. has a way of demeaning one person or the other’s accomplishments. Just because my friend pulled in over 6 figures last year doesn’t mean that he is more successful than I am. It just means his incoming revenue from salary is higher. Instead talk about where people have their money stored. Is it in a savings account (bad)? Is it invested? Are they investing it wisely (for instance not spending money on speculative marijuana stocks)? What are their interest rates for their debt? What are their plans to pay off that debt? All of these are conversation starters that focus on actions people can take not just focusing on the dollar amount in their accounts.

3. Talk about the impact of a lost job – The Covid-19 quarantine serves as a great reminder that we need to have a plan ready should we lose our primary source of income. What a great time to have those conversations now. Things to bring up, “How long can we survive without our primary source of income?”, “What assets could we sell if we had to?”,”What could potentially be an alternative source of income for our family?”, “Should something happen to one of us do we have insurance or a will in place?”. Times like these provide us an all to real example that our day to day lifestyle can be temporary. It is better to prepare for those dire times now while we are relatively safe.

4. Learn what costs are essential in your life – As society strips down all to just essential businesses in operation we can also do the same in our financial life. What a great time to see what you physically must spend money on versus what is just fun to spend money on. During this time I have realized how much money I spend eating out, traveling, going to breweries, etc. These are all hobbies of mine and I’ve known that I spend money on them but during this quarantine I have felt first hand how much I have truly spent on them. It’s leading me to question how much I am spending. Yes I will go out to eat in the future and yes I will travel and go to microbreweries, but now I am aware that I can curb those things. It also has me realizing how much I am spending on gas and purchases I make in the gas station. Use this quarantine to talk with your family about what expenses you can permanently remove from your day to day lives.

5. Find a financial mentor – As you are talking about finances and reading through various websites and books it is important to also find a person that you trust that you can look to as a financial mentor. This person doesn’t have to be perfect. Just someone in a similar situation as you that is open to discussing finances. It’s helpful to have that person in a similar walk of life to bounce ideas off of. The Professor and I chat finances daily. Most of it is nonsense about what the markets are doing or what we think the future might hold but it’s helpful to have the person to bounce ideas of investments off of and someone that will tell you when a purchase you’re considering is stupid. Also a good idea to chat with someone from a similar walk of life. Conversing with a friend who’s income and expenses are ten times greater than yours might just lead to frustration.

There you have it, 5 ways to start that financial conversation at home and ways that we can use what we are experiencing during shelter in place to help curb our spending and grow our net worth beyond The Covid-19 outbreak of 2020.

Stay Safe and as always…

KEEP STACKIN!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

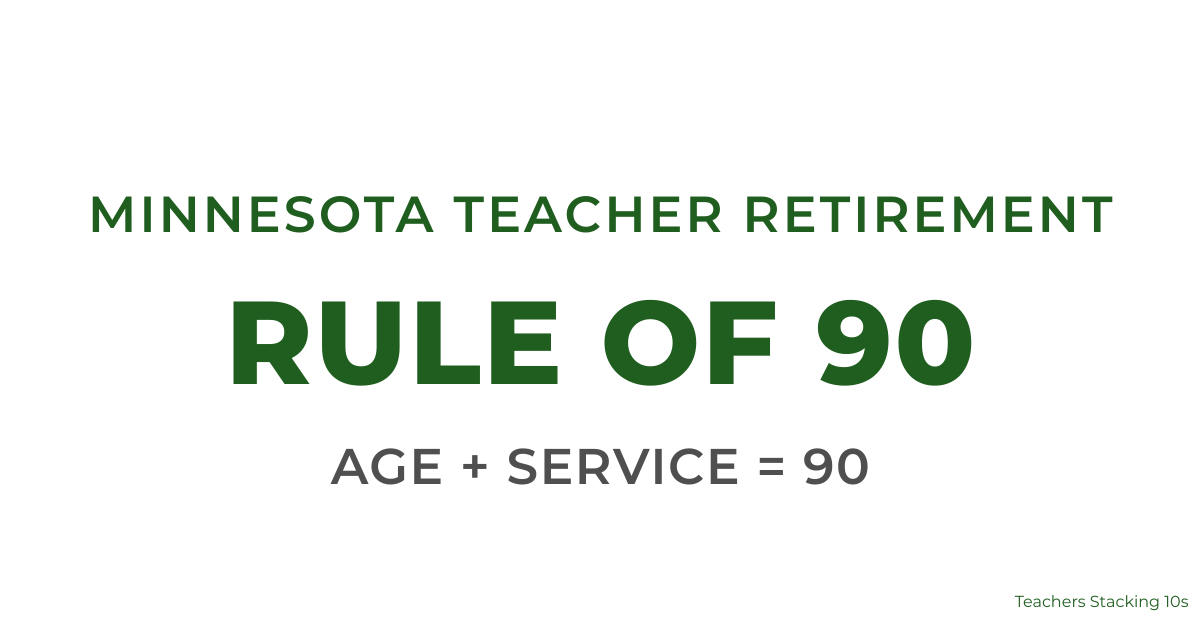

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

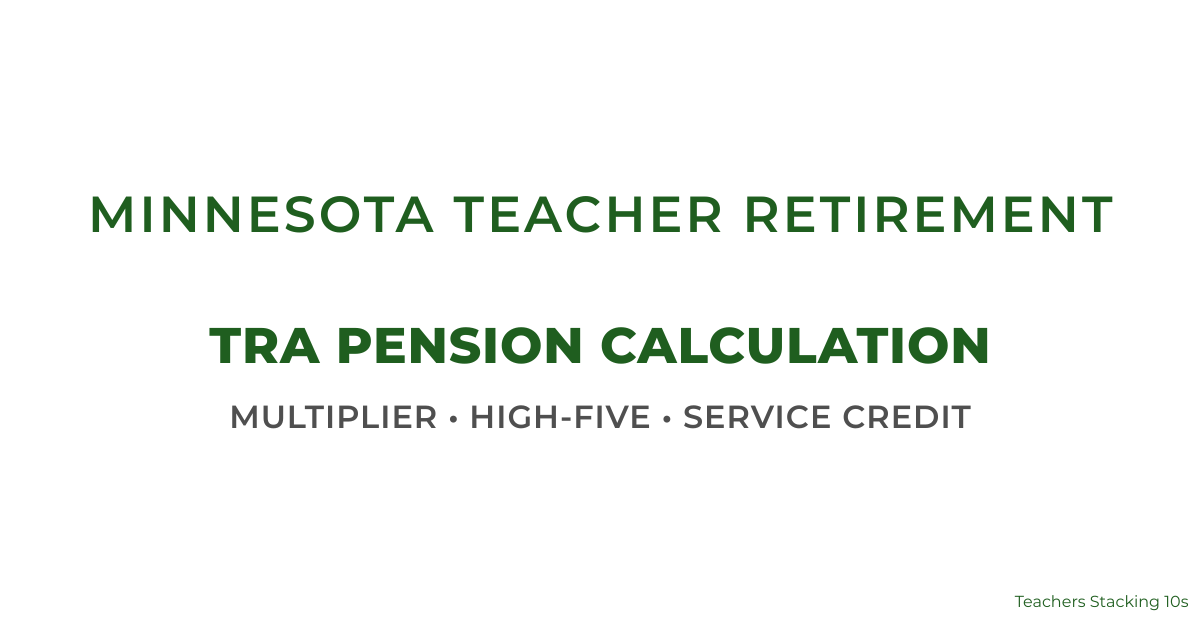

How the Minnesota TRA Pension Is Calculated (Formula, High-5, and Real Examples)

Most Minnesota teachers know they will receive a TRA pension through the

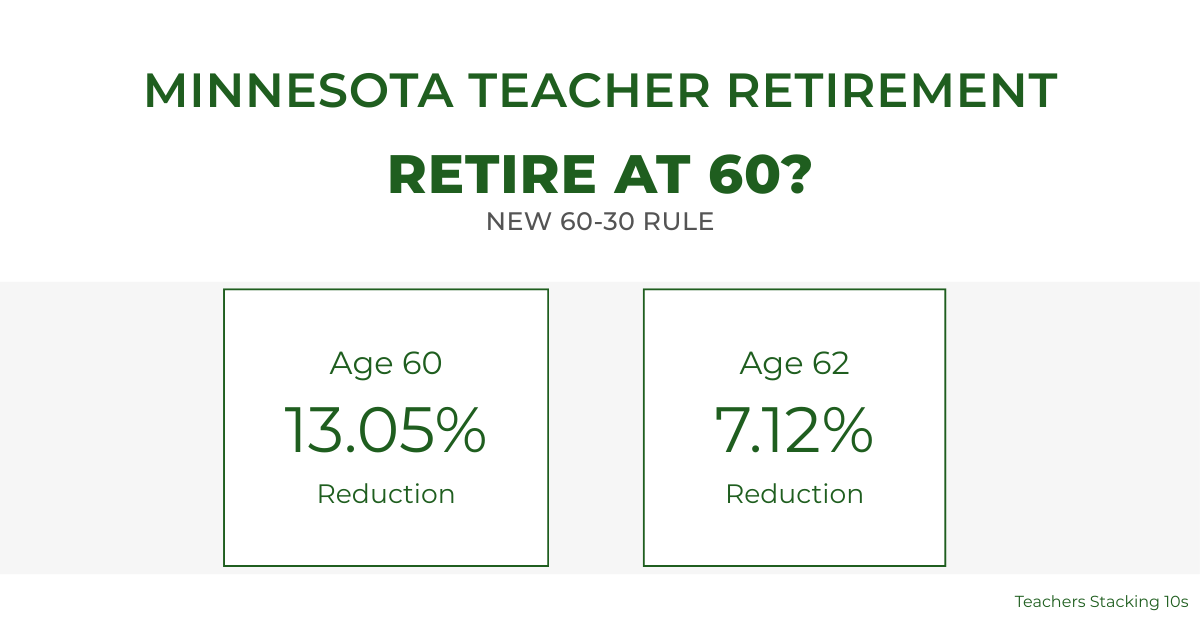

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for