The T.A. and I were talking the other day about the fact that we have talked a lot about what to do once you have money, but many people live paycheck to paycheck. It’s time we talk about the biggest problem facing Americans today…. Debt….

One of the first posts that I read when I started down this path was the classic Mr. Money Mustache post on debt being an emergency. I highly suggest reading that post as Mr. Money has a way with words that I still am learning. He is the man!

When it comes to debt, Americans are in love! According to a 2018 study by Nerdwallet, the average American household has $6,829 of revolving balances each month. Add in your monthly mortgage/rent, car payment, student loan payment, etc… It’s no wonder that your average American looks at you like you have a third arm when you ask them how much they are saving each month for retirement.

If debt is so bad, then why do so many people put themselves in this situation? Most people don’t venture out to bury themselves with debt. It’s more like a death through a thousand paper cuts type of situation. They get that first job and see how much money they are going to be making. They decide to purchase a house to start their family. So starts their life of mortgage payments. They realize they need a new/newer vehicle because they “deserve” it. So they take out a vehicle loan with a monthly payment they can afford. They pick up a few things to go into their house to make it look nicer. They go out to eat a few times a month. All of these small charges go on their credit card because they will have enough money at the end of the month when they get paid. Uh oh, the water heater goes out. $1,200. Damn house. They pay that bill because they have to have hot water, but that means they don’t have enough to pay that $500 credit card bill. It’s ok they think because the minimum payment is only $25. They make that minimum payment and carry over that $475 plus another $15 for a total of $490. Here’s where it all starts to go wrong. They don’t change their habits. They rack up another $500 in credit card charges the next month and now have a $990 bill staring them down. Get the picture?!?

So how do we handle this debt problem? Well, if you’re like most Americans, you ignore it and try not to think about it. You DEFINITELY don’t talk about it. The typical American sticks their head in the sand and hopes the debt will go away. THAT WON’T WORK! So what do they do? They run out and get a consolidation loan or even a home equity loan and pay all them cards off! Problem solved! Wrong. Wrong.

Because here’s what happens. All of their debt is gone, but their habits don’t change. They continue to put those little charges on their credit cards and now, not only do they have that new loan payment, but their credit card debt starts to climb again. It’s an all-too common theme in America. People NOT taking responsibility.

So professor, what’s the answer then? How do I fix this situation?

First, you must face up to your debt and NOT ignore it! Immediately stop spending money on those credit cards. Put every penny you can spare into paying them off. You can start on the card with the smallest balance or the highest interest rate. Hard-core budgeters will tell you it has to be the highest interest rate card, but you need to do whatever works for you! It won’t be easy. It will probably suck, but YOU put yourself into this situation and only YOU can get yourself out.

The key is that you MUST take action.

KEEP STACKIN!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

Minnesota TRA Pension Calculator (High-5 Formula Explained + Examples)

Most Minnesota teachers know they will receive a TRA pension through the

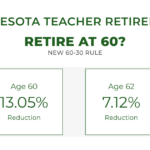

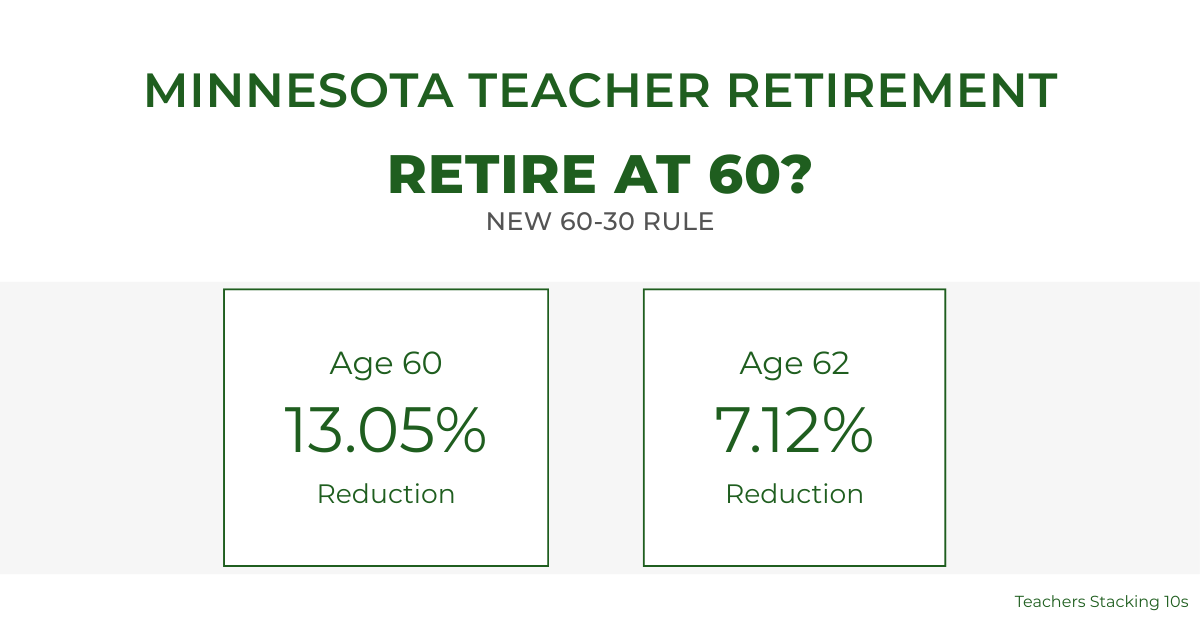

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for