Most Minnesota teachers know they will receive a TRA pension through the Teachers Retirement Association, TRA. Fewer understand exactly how that pension is calculated.

The formula itself is straightforward. The implications are not.

Your TRA pension is determined by three primary variables: your multiplier, your total years of service credit, and your High-5 average salary. Every retirement decision you make, whether you retire at 60, 62, or 65, flows from this base calculation.

Before early retirement reductions are applied, before 60/30 adjustments are considered, and before cost-of-living factors come into play, the core formula looks like this:

Multiplier × Years of Service × High-5 Average Salary

Understanding how each of those components works is critical. Small changes in years of service or final average salary can shift your lifetime benefit by tens of thousands of dollars.

This article breaks down the Minnesota TRA pension formula step by step. We will walk through exactly how your benefit is calculated, what counts toward service credit, how High-5 salary is determined, and how early retirement reductions are applied.

If you are trying to answer the question, “What will my pension actually be?”, this is where the math begins.

If you are a teacher that qualifies for Rule of 90, make sure to check out our full guide, here.

At its core, the Minnesota TRA pension formula is straightforward.

Your annual unreduced pension is calculated as:

Multiplier × Years of Service × High-5 Average Salary

For Tier II teachers, the multiplier depends on when your service was earned.

• Service earned before July 1, 2006 uses a 1.7 percent multiplier.

• Service earned on or after July 1, 2006 uses a 1.9 percent multiplier.

That means each year of teaching does not necessarily earn the same percentage. Your benefit is calculated by applying the appropriate multiplier to each block of service credit.

Here is a simplified example.

Suppose you have:

• 10 years of service earned before July 1, 2006

• 20 years of service earned after July 1, 2006

• A High-5 average salary of $85,000

First calculate the percentage earned from each service period.

Pre-2006:

1.7% × 10 years = 17%

Post-2006:

1.9% × 20 years = 38%

Total earned percentage:

17% + 38% = 55%

Now apply that total percentage to your High-5 salary.

0.55 × $85,000 = $46,750 per year

That $46,750 is your unreduced annual lifetime pension benefit at normal retirement age before any early retirement reductions are applied.

This is why service timing matters.

Two teachers with the same number of total years can have slightly different pension percentages depending on when those years were earned. The multiplier difference may look small, but over 30 years it compounds meaningfully.

Before discussing early retirement options like the enhanced 60/30 rule, it is essential to understand this base calculation. Every reduction percentage is applied after this number is determined.

After calculating your base benefit, the next step is understanding how early retirement reductions affect that amount.

What Counts as Years of Service?

Your total years of service credit is the second major driver of your pension.

Under TRA, service credit is generally earned for each year you work in a TRA-covered position. If you work full time for the entire school year, you typically earn one full year of service credit.

Part-time service is prorated. If you work at 50 percent of a full-time equivalent position, you earn half a year of service credit for that year. The percentage of your contract directly affects how much service credit you accumulate.

This matters more than many teachers realize.

Every additional year increases your total earned percentage under the formula. Because post-2006 service earns 1.9 percent per year, each additional year now adds nearly two percent of your High-5 salary to your pension.

Using the earlier example of an $85,000 High-5 salary:

One additional post-2006 year adds:

1.9% × $85,000 = $1,615 per year

That increase is permanent and paid for life.

Over a 25-year retirement, that single additional year could produce more than $40,000 in additional lifetime pension payments. That is why retirement timing decisions often come down to small service differences. Retiring one year earlier does not just mean one less paycheck. It can mean a permanently smaller pension.

Service credit can also include purchased service in certain situations. Teachers may be able to purchase eligible prior service, such as previously refunded Minnesota service or qualifying military time. Once approved by TRA, purchased service increases your total years of credit and is included in the pension formula calculation.

It is important to verify your official service credit record directly with TRA before making retirement decisions. Small discrepancies can meaningfully change your projected benefit.

A brief note on vesting. Minnesota TRA has relatively accessible vesting rules compared to many states. Once you are vested, you qualify for a lifetime pension benefit based on your earned service credit.

If you leave Minnesota teaching after becoming vested, you generally have a decision to make. You can leave your contributions in the system and qualify for a deferred lifetime pension at retirement age, or you can request a refund of your employee contributions. That refund decision has long-term implications and is best evaluated carefully, but it is separate from how the pension formula itself is calculated.

Service credit is not just a milestone. It is the engine of your defined benefit plan.

How Your High-5 Average Salary Is Determined

The third component of the TRA formula is your High-5 average salary.

Under Minnesota TRA, your pension is based on the average of your five highest consecutive years of salary. “Consecutive” is the key word. The years must follow one another without interruption.

TRA reviews your salary history and identifies the five consecutive years that produce the highest average. That average becomes the salary base used in the pension formula.

For example, suppose your final five consecutive salaries were:

Year 1 – $78,000

Year 2 – $80,000

Year 3 – $83,000

Year 4 – $86,000

Year 5 – $89,000

Add those five years together:

$78,000 + $80,000 + $83,000 + $86,000 + $89,000 = $416,000

Divide by five:

$416,000 ÷ 5 = $83,200

Your High-5 average salary would be $83,200.

That number, not your final salary alone, is what feeds into the pension formula.

This is why late-career salary movement matters.

Lane changes, advanced degrees, and contract increases in your final years can materially shift your High-5 average. Even a $2,000 annual increase sustained over five years can meaningfully change your lifetime pension benefit.

It is also important to understand that only pensionable earnings count toward your High-5. Not all compensation necessarily qualifies. Supplemental pay and other additional earnings may or may not be included depending on TRA rules and how the compensation is structured.

Because High-5 must be consecutive, timing matters. A single lower salary year in the middle of an otherwise strong stretch can reduce the overall average.

This is especially important if you are considering moving to part-time status late in your career. A reduced contract percentage during one of those five consecutive years will lower the High-5 average. That may be acceptable if you are comfortable with where your High-5 already sits, but it should be evaluated before making a schedule change.

When teachers say, “My pension is based on my last salary,” that is not technically correct. It is based on your highest five consecutive years averaged together.

Understanding that distinction helps you make informed decisions in your final career years.

Step-by-Step Pension Calculation Examples

Now let’s walk through three realistic scenarios to show how the formula works in practice.

These examples assume Tier II rules and include both pre-2006 and post-2006 service. The age at which you begin collecting benefits relative to TRA’s normal retirement age determines whether your calculated pension is reduced.

Scenario 1: 40 Years of Service, Retiring at Age 65

Consider a teacher who began teaching at age 25 and retires at 65 with 40 years of service.

Assume:

• 10 years earned before July 1, 2006 at 1.7%

• 30 years earned after July 1, 2006 at 1.9%

• High-5 average salary of $95,000

• Retirement at age 65

Step 1: Calculate earned percentage.

Pre-2006:

1.7% × 10 = 17%

Post-2006:

1.9% × 30 = 57%

Total earned percentage:

17% + 57% = 74%

Step 2: Apply percentage to High-5 salary.

0.74 × $95,000 = $70,300 per year

This teacher would receive approximately $70,300 annually as an unreduced lifetime pension at age 65.

That is what a full 40-year career produces under the current multiplier structure.

Scenario 2: 36 Years of Service, Retiring at Age 60 Under 60/30

Now consider a teacher who began teaching at age 24 and retires at age 60 with 36 years of service.

Assume:

• 10 years pre-2006 at 1.7%

• 26 years post-2006 at 1.9%

• High-5 average salary of $90,000

• Retirement at age 60 under the enhanced 60/30 rule

Step 1: Calculate earned percentage.

Pre-2006:

1.7% × 10 = 17%

Post-2006:

1.9% × 26 = 49.4%

Total earned percentage:

17% + 49.4% = 66.4%

Step 2: Apply to High-5 salary.

0.664 × $90,000 = $59,760 per year (unreduced base)

Step 3: Apply the 60/30 reduction of 13.05%.

$59,760 × (1 − 0.1305)

= $51,961 per year

Even with the early retirement reduction, this teacher would receive nearly $52,000 annually.

Compared to Scenario 1, retiring five years earlier reduces the annual benefit by roughly $18,000 per year.

That is the tradeoff between retiring earlier and allowing the multiplier and service credit to compound longer.

Scenario 3: 25 Years of Service, Retiring at Age 62 Without 30 Years

Now consider a mid-career teacher who retires at age 62 with only 25 years of service.

Assume:

• 5 years pre-2006 at 1.7%

• 20 years post-2006 at 1.9%

• High-5 average salary of $85,000

• Retirement at age 62

• Does not meet the 30-year threshold

Step 1: Calculate earned percentage.

Pre-2006:

1.7% × 5 = 8.5%

Post-2006:

1.9% × 20 = 38%

Total earned percentage:

8.5% + 38% = 46.5%

Step 2: Apply to High-5 salary.

0.465 × $85,000 = $39,525 per year (unreduced base)

Step 3: Apply the Tier II “No Career Rule” reduction at age 62.

From the reduction schedule, the age 62 reduction without meeting 30 years is 21%.

$39,525 × (1 − 0.21)

= $31,225 per year

That is less than half of the benefit in Scenario 1.

This example illustrates how both service length and eligibility thresholds dramatically change outcomes.

Years of service, multiplier timing, retirement age, and the 30-year rule all interact to determine your final pension.

The formula is straightforward. The decisions are not.

Comparing Lifetime Payouts and the Break-Even Question

Now let’s compare Scenario 1 and Scenario 2 more directly.

Scenario 1

Retires at 65 with $70,300 per year.

Scenario 2

Retires at 60 with $51,961 per year.

First, consider the five years between age 60 and 65.

The teacher retiring at 60 collects:

$51,961 × 5 = $259,805

The teacher waiting until 65 collects nothing during those five years.

So by age 65, the early retiree is ahead by approximately $260,000 in pension payments.

However, beginning at age 65, the teacher who waited is receiving:

$70,300 − $51,961 = $18,339 more per year.

Now we can estimate a break-even point.

To “make up” the $259,805 collected earlier, the higher annual pension must close that gap.

$259,805 ÷ $18,339 ≈ 14.2 years

That means the break-even point occurs roughly 14 years after age 65, or around age 79.

If both teachers live beyond 79, the teacher who waited until 65 will collect more total lifetime pension dollars.

If both pass away before approximately age 79, the teacher who retired at 60 will have collected more in total pension benefits.

This does not account for:

• Investment of early payments

• Continued salary earned from 60 to 65

• COLA timing differences

• Healthcare cost differences

But it illustrates the core tradeoff.

Retiring at 60 does not automatically mean you lose money. It changes the timeline of how money is received.

Waiting until 65 increases your annual benefit permanently. Retiring at 60 gives you five additional years of income and freedom.

The decision is not purely mathematical. It is personal, financial, and health-dependent.

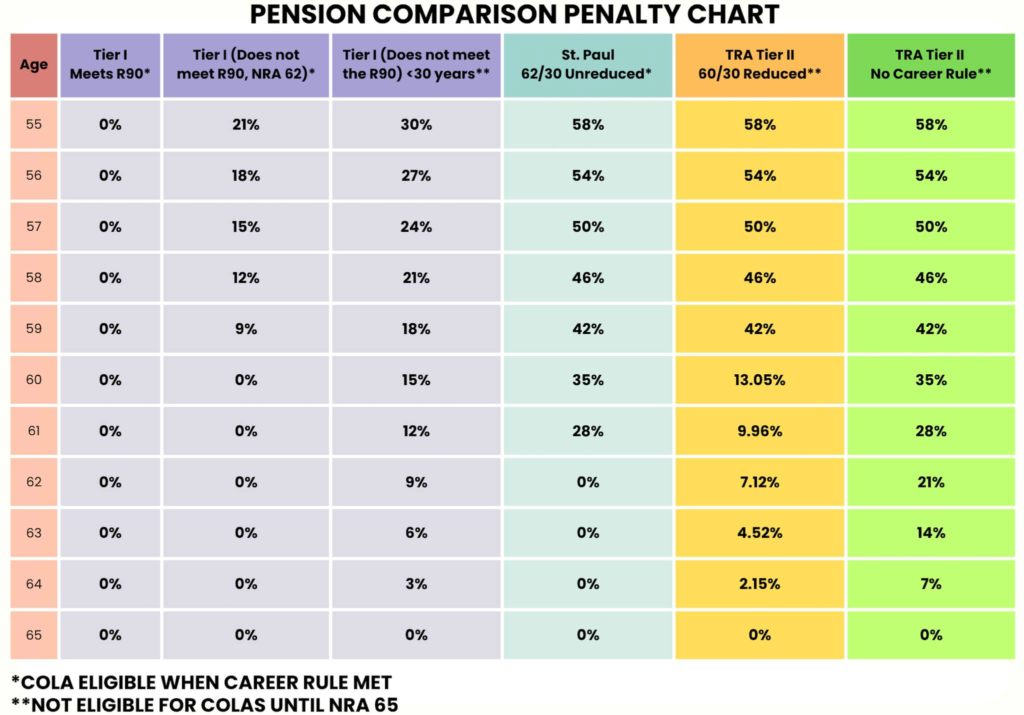

How Early Retirement Reductions Are Applied

The TRA formula determines your base pension first. Early retirement reductions are applied after that base amount is calculated.

If you retire before normal retirement age, your benefit is permanently reduced based on your age and whether you meet specific eligibility thresholds.

For Tier II teachers:

• Meeting the 30-year requirement qualifies you for the enhanced 60/30 reduction schedule.

• Not meeting 30 years places you under the standard “No Career Rule” reduction schedule.

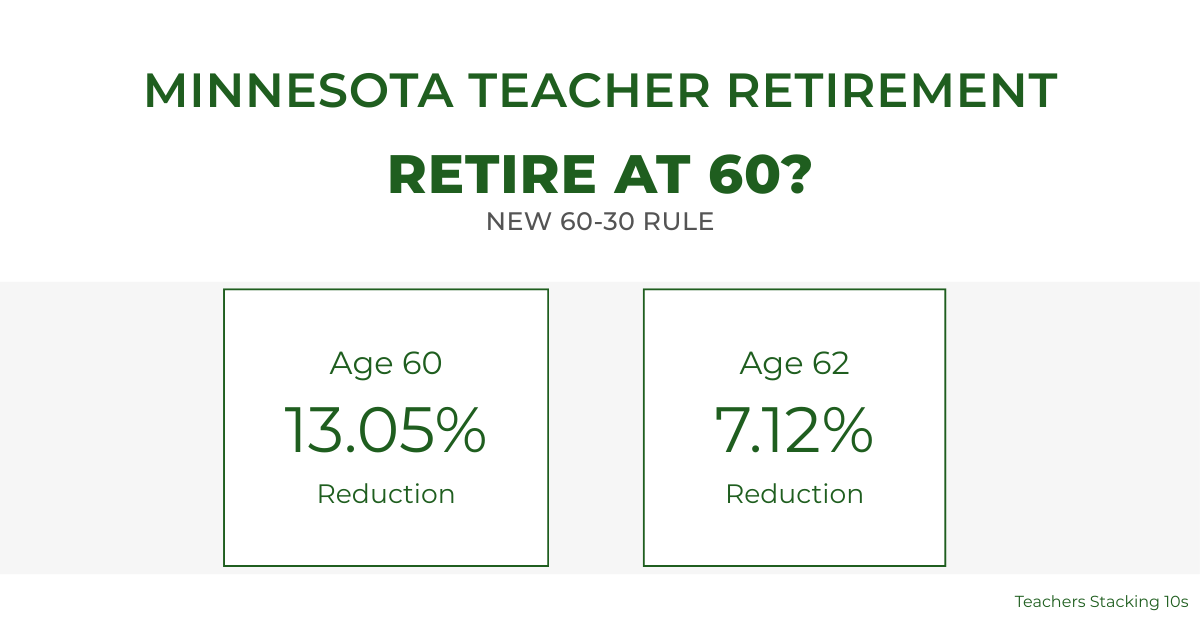

The difference between those schedules can be significant. At age 60, the reduction is 13.05% if you meet 30 years. Without 30 years, the reduction at age 60 is 35%.

These reductions are permanent. They do not disappear at age 65.

For a full breakdown of the enhanced 60/30 schedule and how it compares across ages, see our detailed 60/30 guide.

Understanding this structure is critical. The base formula determines how much you have earned. The reduction schedule determines how much you actually receive.

What This Means for Your Retirement Planning

If you are more than 10 years from retirement, focus on two levers:

• Growing your High-5 salary

• Continuing to build service credit

Those two variables drive the formula more than anything else.

If you are within five years of retirement, model multiple retirement ages. Compare 60, 62, and 65. Small differences in service and reduction percentages create large lifetime differences.

If you are approaching 30 years of service, eligibility thresholds matter. Crossing that 30-year mark can significantly change the reduction schedule applied to your pension.

If you are under 30 years and considering early retirement, run the reduction math carefully. The difference between meeting and not meeting that threshold can be dramatic.

The TRA pension formula is simple. The decision about when to retire is not.

Understanding your multiplier, service credit, High-5 average, and reduction schedule gives you the framework to make that decision with clarity.

If you want a broader overview of how Minnesota teacher retirement works, including eligibility structures and legislative changes, review our complete Minnesota Teacher Retirement guide.

KEEP STACKIN!

Frequently Asked Questions About Minnesota TRA Pension Calculations

Does coaching pay count toward my High-5 salary?

Only compensation classified as pensionable earnings under TRA rules is included in your High-5 average. Not all supplemental pay automatically qualifies. Review your contract structure or confirm with TRA if you are unsure.

Can I estimate my pension before I reach 30 years of service?

Yes. The formula applies at any service level. Multiply your credited years by the appropriate multiplier and apply your High-5 average. Early retirement reductions would apply if you retire before normal retirement age.

Is the multiplier guaranteed?

The current multipliers are 1.7% for pre-2006 service and 1.9% for post-2006 service under Tier II. Pension systems are subject to legislative change, but benefits are calculated according to the law in effect at the time of retirement.

What happens if I leave teaching before reaching 30 years?

If you are vested, you may leave your contributions in TRA and qualify for a deferred pension at retirement age, or you may request a refund of your employee contributions. Not meeting 30 years primarily affects which early retirement reduction schedule applies.

Does working part-time near retirement permanently reduce my pension?

Potentially. Because your High-5 must be five consecutive years, a reduced contract percentage during those years can lower your average salary and therefore your pension. This should be evaluated before changing contract status late in your career.

Leave a Reply

You must be logged in to post a comment.