For years, Minnesota teacher retirement at age 60 was financially unrealistic for most Tier II educators.

If you were hired on or after July 1, 1989, you fell under Tier II rules. You could qualify for the 62/30 provision, meaning you were at least age 62 with 30 years of service, and you would receive a more favorable reduction schedule than the standard early retirement penalties.

But age 60 was not part of that structure. Retiring at 60 meant falling under the harsher “No Career Rule” reduction schedule. For many teachers, that penalty was simply too steep.

In May 2025, that changed.

Minnesota enacted an enhanced 60/30 rule within the Teachers Retirement Association, TRA. The 60/30 option primarily applies to Tier II members who do not have access to the Rule of 90. If you are unsure which tier you are in, review the Minnesota TRA Tier I vs Tier II breakdown first.

This change lowered the career-rule threshold from 62 to 60.

Who Qualifies for the Enhanced 60/30 Rule?

The enhanced 60/30 provision applies to:

• Tier II teachers

• At least 30 years of TRA service credit

• Age 60 or older

If you do not yet have 30 years of service, this rule does not apply.

If you are Tier I, you are governed primarily by Rule of 90 provisions instead. Check out our full guide on Rule of 90 to see those rules.

Service credit generally includes years worked under TRA-covered employment. Purchased service and certain credited time may count, but you should verify your individual record directly with TRA.

What Existed Before: The 62/30 Structure

Before the 2025 reform, Tier II teachers with 30 years of service qualified for a more moderate reduction schedule beginning at age 62.

At age 62, the reduction was significantly smaller than the general early retirement penalty. That made 62 a practical target retirement age for many long-career educators.

However, retiring at age 60 still triggered the standard Tier II “No Career Rule” reductions.

Under that prior structure:

Age 60 carried a 35 percent reduction.

Age 61 carried a 28 percent reduction.

Age 62 under the general schedule was 21 percent, though the 62/30 provision improved that for career teachers.

The gap between 60 and 62 was large enough that most teachers simply waited.

What Changed Under the Enhanced 60/30 Rule

The 2025 legislation lowered the career-rule threshold from 62 to 60 for teachers with at least 30 years of service. The 60/30 provision creates eligibility at age 60, but reduction rules are still tied to normal retirement age.

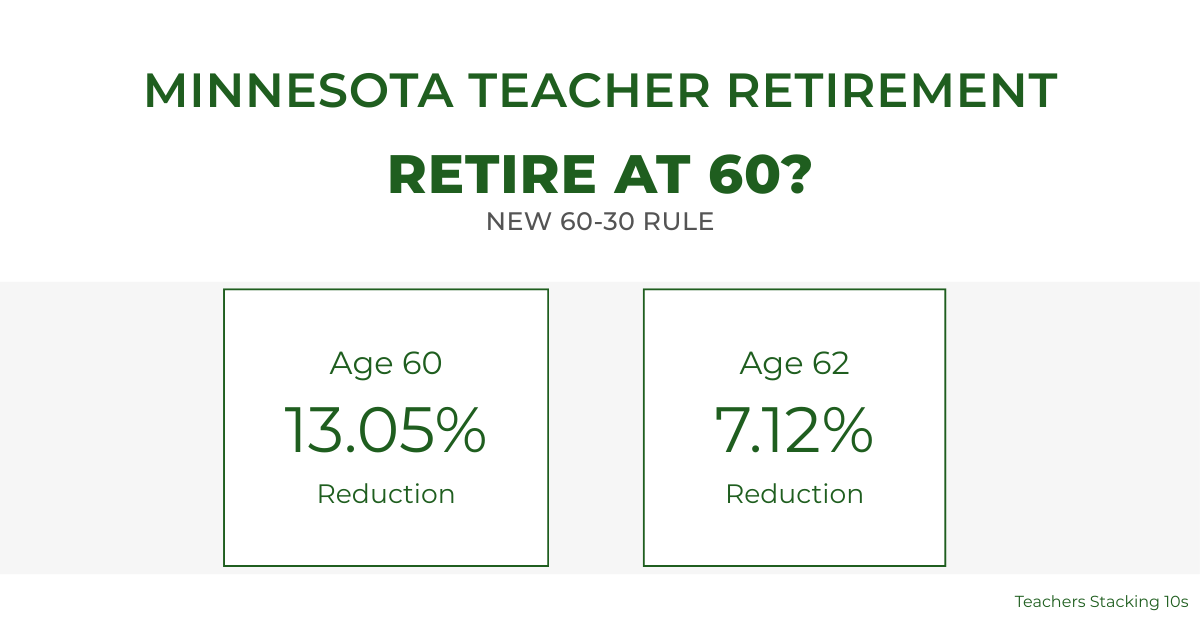

The new reduction schedule for 30-year career teachers is:

Age 60 – 13.05 percent reduction

Age 61 – 9.96 percent reduction

Age 62 – 7.12 percent reduction

Age 63 – 4.52 percent reduction

Age 64 – 2.15 percent reduction

Age 65 – 0 percent reduction

This replaces the much steeper early retirement factors that previously applied at ages 60 and 61.

In practical terms, Minnesota teacher retirement at 60 is now financially realistic in a way it was not before.

Although the 60/30 provision enhances eligibility for certain members, retiring before full retirement age may still trigger age-based reductions. Review our early retirement reduction guide for full details.

How the TRA Formula Still Works

The 60/30 rule does not change the underlying TRA formula. It only changes the reduction factors.

Your base pension is calculated as:

Multiplier × Years of Service × High-5 Average Salary

For Tier II teachers, the multiplier is 1.7 percent for years of service pre-2006 and 1.9 percent for years of service post-2006.

Example:

If your High-5 salary average is $80,000

And you have 30 years of service

Your unreduced annual pension would be:

0.017 × 30 × $80,000

= $40,800 per year

If you retire at 60 under the enhanced 60/30 rule, that benefit is reduced by 13.05 percent.

$40,800 × (1 − 0.1305)

= approximately $35,475 per year

The reduction is permanent. It does not disappear at 65.

Before applying early retirement reductions, your base pension is determined by the TRA formula. If you need a full breakdown of how that formula works, including multiplier and High-5 calculations, see our detailed calculation guide.

What This Means in Dollars

Suppose your projected unreduced pension at 65 is $60,000 per year.

Under the old Tier II early retirement schedule, retiring at 60 could have reduced that to approximately $39,000 annually.

Under the enhanced 60/30 rule, the 13.05 percent reduction would bring it to roughly $52,170.

That difference fundamentally changes the retirement conversation.

Instead of asking, “Can I afford to lose 35 percent?” the question becomes, “Is a 13 percent reduction worth gaining two years of time?”

60 vs 62: The Real Decision

At age 60, the reduction is 13.05 percent.

At age 62, it is 7.12 percent.

That is roughly a 6 percentage point difference.

Two additional years of salary also increase your High-5 average and your years of service, which increases the base benefit before reductions are applied.

In many cases, waiting until 62 produces a noticeably higher lifetime benefit.

However, the flexibility at 60 is now meaningful. For teachers with strong supplemental savings or personal reasons to step away earlier, the financial tradeoff is no longer extreme.

Important: COLA Eligibility Still Begins at 65

Even under the enhanced 60/30 rule, cost-of-living adjustments typically do not begin until normal retirement age, generally 65.

If you retire at 60, you may receive several years without COLA increases. Inflation during that period affects long-term purchasing power.

The reduction schedule improved. COLA timing did not.

Health Insurance Between 60 and 65

One of the most overlooked pieces of retiring at 60 is healthcare.

Medicare eligibility begins at 65.

If you retire at 60, you must bridge five years of coverage. That may include:

• District retiree coverage

• COBRA

• Spousal coverage

• Individual marketplace plans

Healthcare costs during that window can materially impact whether retiring at 60 makes sense.

The Bigger Retirement Strategy

The enhanced 60/30 provision is a meaningful improvement for Tier II educators. It narrows the gap between career teachers hired before and after 1989 and expands retirement flexibility.

However, your TRA pension is only one part of your plan.

Your 403(b) balance, Roth IRA contributions, savings rate, and overall retirement readiness determine how much flexibility you truly have.

Minnesota teacher retirement at 60 is now possible for many educators.

Whether it is optimal depends entirely on your numbers.

If you need a full breakdown of how the TRA formula works and how to project your benefit, start with our complete Minnesota Teacher Retirement guide.

Keep Stackin!

Frequently Asked Questions About the Minnesota 60/30 Rule

Can I retire at 60 with less than 30 years of service?

No. The enhanced 60/30 rule requires at least 30 years of TRA service credit. If you retire at 60 with fewer than 30 years, you will fall under the standard early retirement reduction schedule, which carries significantly larger penalties.

Is the 13.05 percent reduction permanent?

Yes. The reduction applied at age 60 is permanent. It does not disappear at age 65. Your pension is reduced for life based on the age at which you begin collecting benefits.

Does the 60/30 rule apply to Tier I teachers?

No. Tier I teachers are primarily governed by Rule of 90 provisions and different retirement eligibility rules. The enhanced 60/30 change specifically affects Tier II teachers with at least 30 years of service.

Does sick leave count toward the 30 years of service?

Generally, sick leave conversion can increase your service credit at retirement, but eligibility rules and calculations can vary. You should verify your official service credit total with TRA before making a retirement decision.

Does coaching pay or extra duty pay count toward my High-5 salary?

Only earnings that are considered pensionable compensation under TRA rules are included in your High-5 average salary calculation. Not all supplemental pay qualifies. It is important to confirm what counts toward your final average salary.

Can I continue working after retiring at 60?

There are restrictions on returning to work in a TRA-covered position after retirement. Earnings limits and reemployment rules may apply. Before retiring and returning to work, review TRA guidelines carefully.

Will the 60/30 rule change again in the future?

Pension systems are subject to legislative changes. While the enhanced 60/30 rule is currently in effect, future reforms are always possible. Retirement decisions should be based on current law, but awareness of legislative risk is prudent.

Leave a Reply

You must be logged in to post a comment.