Credit cards… For some people, they are a symbol of debt, despair, and frustration. For others, they are a symbol of income, joy, and motivation. How could a small piece of plastic stir such different emotions in people. For this answer, we need to analyze how people deploy these cards in their lives.

The Good

Let’s start with those people that use credit cards to the benefit of the holder. In recent years, credit cards have worked hard to recruit new card owners by offering some great sign-up bonuses. These various bonuses include; cash-back and match rewards, travel miles, and card points that may be redeemed for gift cards or other redemption portals. Some of these bonuses are one-time hits for meeting certain spending requirements. For example, I just recently met my spending requirement on my Chase Sapphire Preferred card. The spending requirement was $4,000 in the first 3 months of card ownership. By meeting this requirement, I was awarded 60,000 bonus points. (I will do an in-depth case study on this card in a future post.) Others are continuous bonuses that are earned each time you spend money on the cards. My case study on the Discover It card was an example of a cash-back card. These people are go-getters that think about what they want and find a way to make it work for them. Credit cards are a means to an end for them. The most important thing about these people is that they pay their statement balance in full each month. They do NOT pay interest to the credit card companies. That would defeat the purpose of getting those bonuses because the company might pay you a 2% cash-back match for your spending, but they will charge you in excess of 25% interest if you carry that balance forward!

I am one of these people, but I wasn’t always….

The Bad

The next group of people are those that use cards to pay bills, expenses, and other items both necessary and unnecessary. These people do not plan their spending on their cards. They lose out on getting great bonuses. These aren’t bad people. In fact, I used to be one of them, and I’m not half-bad (at least according to my wife). They just need a little guidance and direction. One important thing that this group needs to improve upon is creating and sticking to a budget, as you can see here. This step in the process can be a very difficult one because people at this stage have probably never used a budget before. They have just spent money as they needed it. This is the point where you become proactive instead of reactive with your money. These people end up paying that 25% interest on their cards because they can’t quite afford to pay the full statement balance. They “justify” carrying that balance because the interest might only be $25/month. This is the “monthly payment” mindset that I will touch on more later in this post.

The Ugly

This final group of people are ones that take spending on their credit cards to the extreme. Not only do they pay their bills on their cards, but they also put unneeded expenditures on them. The biggest problem is that this group has one or more maxed out credit cards with not enough cash to pay them off in the next month, or in some cases, in the next few years! They end up paying hundreds, or even THOUSANDS of dollars every year in interest! They are GIVING money to these credit card companies. Credit cards for this group cause fear and anxiety. You can’t talk with these people about credit cards and responsible spending because they become angry and defensive. I’ve tried to have small conversations with some of my closest friends about this, but I’ve learned that it’s not a topic that people are comfortable talking about. I’ve gotten to the point that I don’t even talk about our financial situation with others unless they ask, and even then I just say that we don’t have any credit card debt and if they ask, explain how we were able to accomplish this.

I feel bad for many of the people in this group, and I don’t want to come across as callous, but honestly, it’s usually their own fault. I realize that there are things like medical emergencies that can destroy and families’ financial future, but those are the exceptions and not the norm.

So how did we go from the ugly to the bad to the good???

The Process

The first step for us was to actually realize what we were doing was stopping us from doing the things we dreamed about doing and our retirement goals. I studied our monthly spending and realized that we were losing over $250/month to credit card interest!!! We were so stupid, but the thing is.. we could afford our monthly payments. We weren’t adding anymore to our debt, but we just weren’t really digging our way out. This is true of most Americans. We have been trained to think monthly payments are required. MONTHLY PAYMENTS are bullshit! If you want to gain financial security, you MUST eliminate the term monthly payment from your vocabulary! The only monthly debt payment you should be making is your mortgage.

Once we admitted our problem, we developed a debt payment plan. We chose a debt snowball strategy. This is where you list all of your debts on a piece of paper in order from smallest to largest. We then proceeded to pay the minimum payments to all debts except for the smallest one. We put as much as we could until it was paid off. We then took that “extra” money and added it to our next smallest debt. We did this for 3 years until we had paid off all $18,000 in credit card debt we had. Now, people will tell you that you should pay off the highest interest debt first. This is really the most efficient way of paying your debt, but my wife and I needed the emotional “win” to keep us motivated in paying our debts. If we would have started with our $9,000 credit card, it would have taken us over 20 months to pay it off. This would have been a long time to wait for a “win”. We may have lost our motivation and slipped back into paying the monthly minimum. We’ve all seen those minimum payment graphs on our credit card statements, so I won’t bore you with that, but you MUST find a way to pay more than the minimum each month on at least one card.

At the end of those 3 years, we had reached the top of the mountain, or so we thought. We had eliminated all of our credit card debt. We had moved from the ugly to the bad. How did we move into the good? I had read various websites like Mr. Money Mustache, and realized I wanted those credit cards, who we had paid so much in interest to, to actually pay us! I chose to start with the Discover It card. I was approved for the card and began paying all of our monthly bills on it. Each month, we paid off the card in full. The KEY is that you MUST pay your statement balance in full each month. If you cannot have the discipline to do this, DO NOT attempt to use this strategy. You’ll end up paying more in interest than you will receive in benefits.

Finally, we had turned the tables on those damn credit card companies. For 25 years, all the way back to that Citibank card that I signed up for on Spring Break back in 1993 (but I got a sweet T-shirt!), I had been paying interest. Now the credit card companies pay us. And you can make your credit cards work for you too! Take that ugly situation, analyze what you can do to fix it, and turn it into a win for you. It may take some time and discipline, but you can do it!

Keep Stackin!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

Minnesota TRA Pension Calculator (High-5 Formula Explained + Examples)

Most Minnesota teachers know they will receive a TRA pension through the

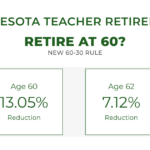

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for

Leave a Reply

You must be logged in to post a comment.