It’s happening! The TA and I are going to be getting Vanguard as a 403(b) vendor in the New Year! Wait, you aren’t as thrilled as we are? You should be. This is great news!

What’s the big deal Professor?

Well, everybody loves saving money! This is what Vanguard is going to do for us. Most teachers don’t realize that a 403(b) vendor charges fees to “advise” you on how to invest your money. Depending on your vendor, these fees can range from $100’s to even $1,000’s of dollars per year. This can cost you MASSIVE amounts of money over the course of your teaching career. Our current vendor charges a fee of 1% to manage our money. I have about $70,000 in my account, so they charge me $700/year! Vanguard charges a $5/month record keeping fee, so my yearly cost will be $60! That’s a savings of $640/year! No matter how much money I add into my account, I will still only be paying $60/year!

There has to be a catch?

Yes. The “catch” is that you can only purchase Vanguard funds. This is fine with the TA and me since we are big fans of Vanguard’s low expense ratio funds. We both actually hold them outside of our 403(b) in personal IRA and taxable accounts.

Friend with benefits

Not only will we save money with Vanguard as our provider, but we will also have more control of where our money goes. With our current vendor, we have to talk with our adviser about where we want our money. We have to tell them the percentages and then we have to listen to them try to “persuade” us to invest in high expense ratio funds. We can log in to see our accounts, but we have ZERO direct control over anything that happens in the account. We have to contact our adviser to make changes. With Vanguard, we will be able to log in and set our investment profile directly.

A typical conversation with my 403(b) rep.

Don’t get me wrong. My adviser is a nice guy and I know he means well, but I’m an intelligent investor and the person I trust most with my money is me. I hope that doesn’t come off as arrogant, but I have put the time in to learn about good investing strategies. You can do it too! Just go back and read our post on understanding stocks, ETFs, and funds.

Remember, an adviser makes his money by telling you what to do with your money. Even if you aren’t confident in making your own money decisions, there are three key questions that need asking.

- What is your company’s expense ratio?

- What is the expense ratio of the funds you are recommending?

- Is there a penalty for moving money from one fund to another?

The first two questions will give you an idea of how much of your money you are losing. If the answer to either of these questions is over 0.50%, then you are being charged too much.

If the answer to the third question is yes, RUN! This will mean your money is in some kind of annuity. These are bad! You should NEVER be penalized or required to keep your money in a fund for a certain amount of time.

The Hurdle

The one hurdle that you have to get past is having limited options when it comes to 403(b) vendors. Every school district has a list of approved vendors. You cannot choose anyone outside of this list to administer your 403(b). The TA and I did not have a great list of vendors available to us, so we decided to ask our school if Vanguard could be added. We were lucky, for us it was simple. We are a small school district, so we don’t use a 3rd party administrator to oversee our 403(b). Our school board quickly approved adding Vanguard. You can try the same thing with your district. Show them the comparisons between a company like Vanguard and your current choices. It can be a powerful influence to show them the amount of money that their employees could be saving.

I just wish I would have learned this 20 years ago!

Keep Stackin!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

How the Minnesota TRA Pension Is Calculated (Formula, High-5, and Real Examples)

Most Minnesota teachers know they will receive a TRA pension through the

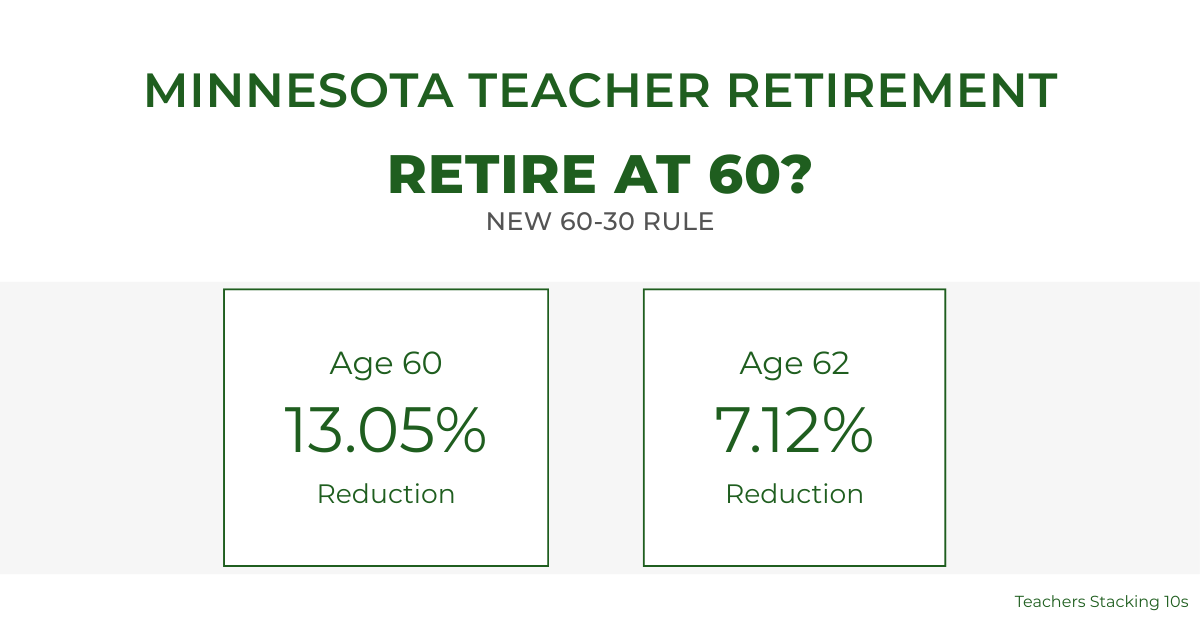

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for

Leave a Reply

You must be logged in to post a comment.