There’s no place like home…. Or is there.

Some people love to travel the world and see different things. I am not one of those people. I am very much a homebody, but as I get older, I am realizing how much I hate the cold winter weather and want to head somewhere warm. This year I decided that my wife and I are going on a vacation. After looking at our budget, I realized that we would have to blow it up to make a nice vacation work. I knew I would have to find a way to pay for it that was “unconventional”. Hello, travel rewards credit cards!

If you’ve been reading this blog, you remember my post on the cash-back Discover It card. After that successful venture, I started doing more research into using credit cards for the travel rewards. I ended up choosing the Chase Sapphire Preferred card for it’s excellent bonus. After spending $4,000 in the first 4 months, I would be eligible to receive 60,000 bonus points. This was easy enough as I had been paying our monthly bills on the Discover It card for the previous year. I just changed those payments over to the Chase Sapphire Preferred card. We easily met that minimum spend in the first 3 months, and BOOM, 60,000 bonus points were added to our account. At that point, I started paying our monthly payments on our Chase Freedom Unlimited card because we earn 1.5 pts for every dollar we spend. Then I transfer those points to my Chase Sapphire Preferred card because those points are worth 1.25 cents/point when redeemed for travel through the Chase portal! Double-hacking!!

An added bonus was you can get 15,000 point for every friend you refer that qualifies for a card. So being the great friend that I am, I referred the T.A. Once he qualified, another 15,000 points were added to my card. I’m such a nice guy!

So after paying our monthly bills over the last 8 months on the Chase cards, we ended up with over 94,000 points!

Monthly spending points – 19,512

Referral – 15,000

Bonus Points – 60,000

Total points – 94,512

After accumulating these points, we decided that we wanted to go to Cabo. We are lucky in the fact that my parents have a timeshare, and we were able to get a FREE 6 night stay at a resort there through my parents’ point portal. I looked into flights and was able to get round-trip flights to Cabo for 91,163 points! FREE FLIGHT!

The Professor taking it all in.

Granted, the die-hard travel hackers out there could have done this more efficiently and for better “value”, but for my first time, I’m pretty happy with the results! Another example of making the credit card companies work for you! And hey if you decide you’d like to try the Chase Sapphire Preferred card. Here’s a referral link that you can use.

KEEP STACKIN!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

How the Minnesota TRA Pension Is Calculated (Formula, High-5, and Real Examples)

Most Minnesota teachers know they will receive a TRA pension through the

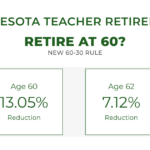

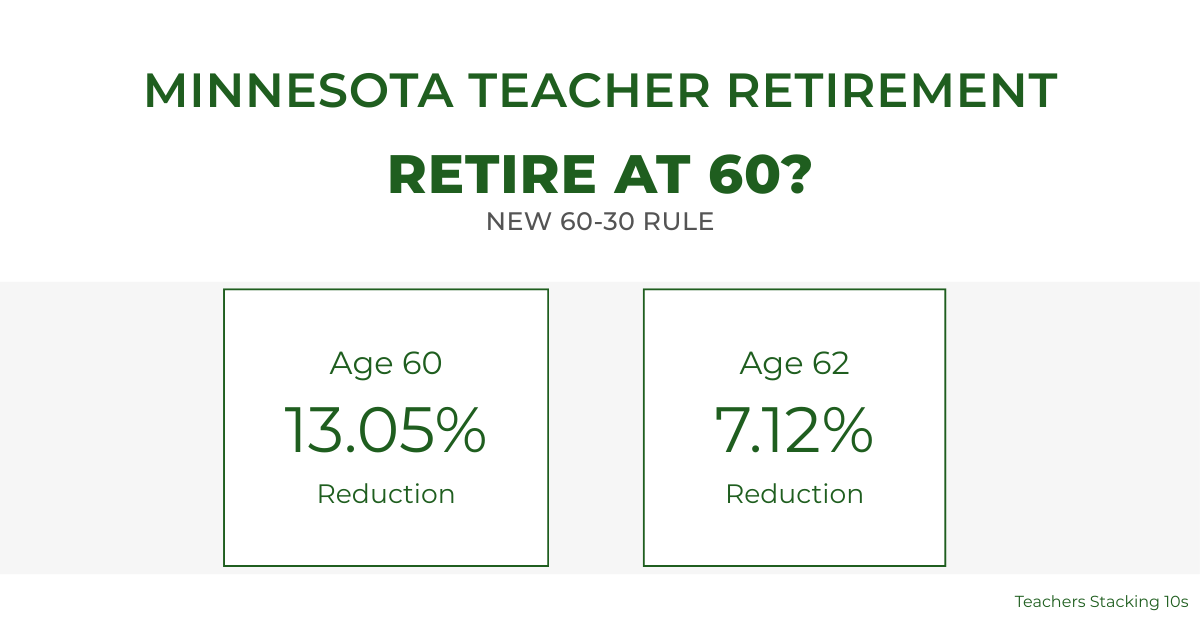

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for