I feel like I need to start this post off by saying that I know that this won’t be for everyone. I have always been a handy person. I’m not saying this to toot my own horn because much of the work that I did, can be done by most people with a little bit of research. With YouTube, you can learn how to do almost anything. One YouTuber that I got a TON of information from was Basement Finishing Guy. His videos were extremely helpful and gave me tons of insight into how to do things correctly.

I’m also very lucky that I have access to most of the equipment that I used. Even if you can’t do all of the work that I did, you could definitely choose parts to tackle yourself and save some money.

This whole project was always something that I always wanted to do, but it took a heavy rainfall last March to push me over the edge. We had gotten some water in the finished side of our basement in the past, but this time it really flooded one corner. If I would have done a little investigating, I would have found that the reason it flooded was because the small window well had filled with water and flooded in through the window. But I was convinced that we had a crack in the cement wall so I just started tearing down the paneling and drywall and framing. Lo and behold, no crack! Well, the carpet still had to come out, so I just went with it. I still wanted to make a larger window in that room and also put a larger window in my daughter’s basement bedroom to make it legal. She’s been in that bedroom for a couple years, and I knew that I would feel more comfortable having a large, legal egress window there, so away I went.

The first stage of the remodel required me to demo the entire family room and one wall in her bedroom. It took some work, but it didn’t require much in terms of “construction” knowledge. I just had to tear out all the old drywall and paneling and remove the carpet and pad. This first picture is the beginning of the tear out phase. This is where the leak occurred. It was a little “rash” on my part to just start tearing things out, but as you can see along the base of the wall, it was only a matter of time before that 2×2 stud was completely rotted out. This wasn’t the first time that water had penetrated into that wall. The picture on the far right is about halfway through the demolition phase.

The second phase of the project was the main reason for the renovation. The installation of the egress windows. As you can see in the pictures above, the previous windows were those small windows that would not allow anyone to escape. This phase of the project did require me to hire a company to do the actual cutting of the concrete. I was able to dig out the “well” for the window before they arrived as they told me, “We just cut. We don’t touch a shovel.” Boy, am I glad I hired them. They showed up with over $150,000 worth of equipment and a saw blade that made my size 12 shoe look like a kid’s toy. They completed the job in less than 2 hours. If I would have tried to cut it myself, they told me that it would have taken me a week and I would have had cuts that were completely unsquare. It ended up costing $1,150, but sometimes you need to bring in the professionals. Once they had cut the openings, I went right to work boxing in the opening with framing and installing the 48″x48″ sliding windows. The pictures below show the hole I dug and filled with 3/4″ rock, the saw blade they showed up with, and how it looked after I got one of the windows installed. Once the inside was finished. I moved to the exterior and installed the egress wells. It just so happened that I did this part on one of the hottest days of the summer, but I knew I wanted to get them in before we got any heavy rains. This was also the most expensive parts of the remodel as I went with a modular type egress system. The total for these was about $1,700. I attached them to the concrete foundation with a hammer drill and some anchor wedges. They turned out fabulous.

Phase three of the project was installing can lights into the ceiling. I installed two rows of four cans separated an equal distance apart. This was a pretty easy installation. The more difficult part was the wiring. I contacted my brother-in-law electrician and we talked through the steps involved. I also watched a YouTube video. It took a solid 3-4 hours, but I was able to get everything wired into place. You can see the picture on the lower left below with the lights installed and on. The hardest part of this phase was the wiring in the box for the switches. I installed the lights so that they were controlled in two zones. The front four lights controlled by one dimmer switch and the back four lights on a separate dimmer switch. Again, speaking with my brother-in-law, I was able to get these lights wired correctly without any real problems.

The next phase was to install insulation on the exterior walls and frame out 2×4 walls. I watched a LOT of different videos to make sure that I framed the walls correctly. As I mentioned before, Basement Finishing Guy on YouTube really has some great videos on this part. I watched his 6-Part Basement Framing Series probably 4-5 times through to make sure I did everything correctly. I started by attaching 2″ rigid foam insulation to the bare concrete with proper adhesive. Once those were attached, I framed the two exterior walls following all the steps that were shown. This is where a remodel project really starts to take shape. There is something about seeing these perfectly straight 2x4s all lined up that is just so satisfying. The picture on the lower left is from the family room, and the lower right is from my daughter’s bedroom.

Once the walls were framed up, I proceeded to attach new outlet boxes to the walls and wire them in. This was much easier than wiring in the can lights. I made sure to check the proper electrical codes and attach the boxes in the proper positions and secure the wires correctly. I only zapped myself one time when I grabbed the old metal box on the sides. It was a small jolt like back when we used to brush up against the electric cattle fence. Once that was complete, I started to hang sheetrock. Doing sheetrock, or drywall, is a pain in the ass. I had to have the TA come over one day to help hang the sheets on the ceiling because each sheet is about 50 lbs. Not only is the stuff heavy, but cutting out for lights and outlets is dusty as heck. A Rotozip tool makes it easy to cut the holes out, BUT it’s also easy to make a mistake as you can see in the picture on the lower left. One thing I would probably do differently if I did it again would be to add furring strips to the ceiling to even out some of the unevenness in the joists. There were a couple of them that caused us some issues during hanging. Even so, it turned out pretty well. As with everything, I watched a lot of videos on how to do the drywall properly. A big help for my was DIY Home Renovision’s Drywall Installation Guide. I watched these videos over and over as well. He’s also got other great videos on things you can do in your home.

Hanging the drywall took a day, and then it was time to mud and tape. This part of the job took me the longest time because it’s very fine work AND you have to give the drywall “mud” time to dry. It’s also TERRIBLY messy, especially when working on the ceiling joints. One YouTuber in particular, Vancouver Carpenter, was a great help in my “mudding” process. The middle two pictures are before I applied mud. The picture on the right is of my “finished” work in the family room.

Next, I primed all the walls with a quality primer/sealer, and then painted. Nothing too exciting there. Then I installed a Dri-Cor subfloor that will prevent the new carpet from getting wet again IF any water does happen to infiltrate the basement. This system involves 2×2 sheets of plywood that have a dimpled plastic laminated to the bottom to keep the organic material off the concrete floor. It also gives some R-value insulation to the floor to make it feel warmer. Again, I found a great video online that helped with this install. This was a pretty simple install as the pieces are tongue and groove. I did attach them to the floor in spots with a hammer drill and concrete screws as per the manufacturer’s instructions since we were going to be installing carpet underneath. Once that was finished, I installed trim and baseboard around the room before the final step.

The final stage of the project was carpet installation. Again, I hired professionals to do this part of the job as it is another pain in the ass to lay carpet and padding out. This was another pretty large cost as we went with a higher quality carpet that will last and be resistant to mold, mildew, and stains. You can see in the two pictures below the before and after carpet look of the room.

It definitely wasn’t a cheap project, but by doing a lot of the work myself, I was able to save a TON of money. My total cost for the project was about $12,000. That’s just for materials and a few tools I used on the project. Most contractors say to find your materials cost and double it to account for labor costs. I did pay for labor for the cutting of the concrete and for the carpet installation. I’d say a fair estimate for the total cost would have been at least $20,000 if I would have hired the whole project out. I’m glad that I did this project last year instead of this year as costs of some building products, especially lumber, have tripled!

All in all, I think the project went very well. I didn’t really mind the electrical work and framing. The drywall and mud/tape was definitely a job that takes some skill and practice to do well. There are spots in my mud job where you can see imperfections, but for the cost, it looks pretty good to me!

This all might seem like a lot of work and really complex, but YouTube can be your best friend. You can learn how to do almost anything by going there and watching videos. The videos I linked throughout this article are the ONLY reason that I was able to tackle this job. I was definitely nervous doing a project of this scope, but as we tell our students, “Knowledge is power.” With the explosion of the Internet the last 20 years, there has never been more knowledge out there available for everyone to take advantage of. That being said, I am NOT affiliated with ANY of the links that I have included in this post. I included them for you to see how easy it is to learn from people that are out there on YouTube.

Hopefully this inspires you to look at your own situation and what you can do in your remodeling projects to save a little money and as always….

KEEP STACKIN!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

How the Minnesota TRA Pension Is Calculated (Formula, High-5, and Real Examples)

Most Minnesota teachers know they will receive a TRA pension through the

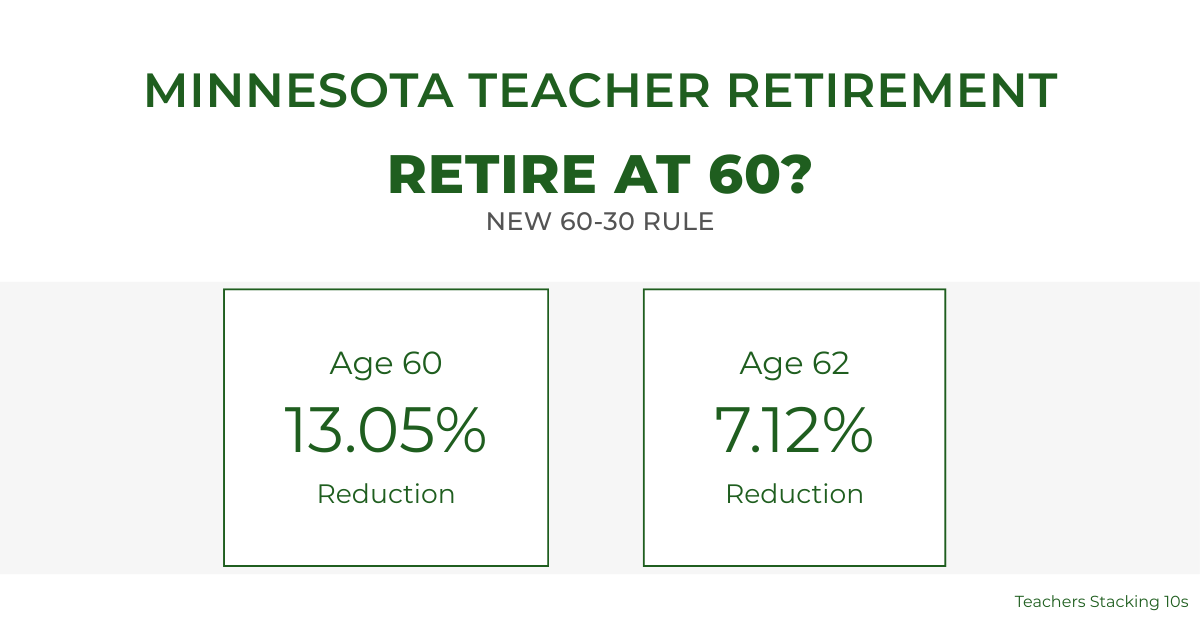

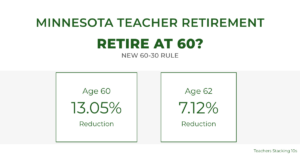

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for