THE SKY IS FALLING! THE MARKET IS CRASHING! CATS AND DOGS LIVING TOGETHER! WHAT SHOULD I DO????!?!?!?!

Step 1 – Relax. DO NOT SELL YOUR STOCKS!

As with anything during these strange times of the corona virus, it is really important to weather the storm. It is a time for patience not panic. We are hoping to clear up some of the big financial questions that we are all asking at this time.

First up – What is a “market crash?”

A market crash is a bit of an exaggerated term. It truly means that the overall value of all the stocks in the market have dropped a significant amount. Currently, in this last full week of March 2020 they are down 33% since the market’s high a few months ago. For many of us, it looks like our investment are way down. There is some truth to this. The index funds I bought in February for $300 a share are now worth closer to $225 a share. So on that investment, yes I am currently behind. But it is important to note that I have purchased a lot of index funds over the years at a variety of different price points. While it does seem like I have lost a lot of money in the short term, I am still up overall. I bought those same index for $160 a share in 2014. So overall, still ahead and I have been collecting dividends on those shares for the past 6 years as well. So despite these times of record losses, I can still sit here and joke around and smile because I understand that this “crash” like all crashes is temporary.

What is a correction? What is a bear market?

Hopefully, as a teacher you aren’t tuned in to the daily back and forth of the stock market. Following the daily ebbs and flows can be draining and can take away from our overall goal. And that is to invest for the long term. If you have been following the talking heads, there is a lot of current talk about a correction and heading into a bear market. A correction is a natural process that occurs in the stock market. Stocks often times are over valued because of record profits and many people buying in when times are good. As a country, the USA had been riding an inflated market for most of Trump’s presidency. President Trump is a business man so much of his team’s focus has been to ensure stock market growth. This lead to a lot of confidence in the economy and lots of buying in the market driving the prices of everything way up. At some point we knew it wasn’t going to last forever. Many individual stocks and funds had become over-valued. Insert an event of uncertainty (A global pandemic) and we get the return back down to normal. Sometimes the correction can send the Stock Exchange into what’s called a bear market. It’s impossible to say for certain if this virus will launch us into a bear market but a lot of people smarter than us say that is likely the case. What does a bear market imply? A bear market is a 20% drop in stocks from their all time high, so yes, we are currently in a bear market. The question that we don’t know the answer to is how long with this bear market last. That will really depend on how long this coronavirus pandemic lasts. It may be surprising to here, but as a young investor, this drop in the market greatly excites me. It will really open the door for our generation to get into the market at a low point and see our wealth accumulate. It’s just unfortunate that it took a crisis like this to cause it. More on that later.

Why you can’t “time” the “crash”.

Many times, I find myself walking the professor back from the metaphorical financial ledge. He is an aggressive investor and wants to accumulate wealth in a hurry. Who can blame him! He doesn’t have a much time as I do to sit back and let those index funds grow. He and others often talk to me about, “Oh if I only knew that this crash was coming I could have sold!” or “Why did I buy those stocks right before the downturn.” Or the best yet, “I don’t want to buy any now until I know it’s hit bottom and is on it’s way back up.” To all of those out there thinking things like this… NO ONE, NOT EVEN PROFESSIONALS CAN TIME THE MARKETS! SO GET THAT IDEA OUT OF YOUR HEAD! Absolutely no one can predict the short term day to day transactions of the markets. Especially not us. So now is a great time to stick to your monthly plan of investing. Whatever you do. DO NOT SELL! It is the worst time to sell your stock, and it is a move of panic. Leave that money in there. The one thing that we can predict about the market is that over time the market goes up. It might not be for a couple of years but it always goes back up. What a great opportunity for us to accumulate some cheap index funds!

What about the different payment options that are being made available for my mortgage, student loans and other expenses.

NO.

If you still have paychecks coming into your household and you don’t have to defer those monthly expenses, don’t. The only thing those are doing is delaying your debt. You’re better off staying on whatever plan you have to pay that debt down versus trying to have more disposable income in your pocket while you are stuck twiddling your thumbs inside. If you don’t have a stable paycheck coming in currently, then obviously you should use common sense. Look at your budget and see if you can afford to keep paying those things or not.

Step 2 – Use this crash to your advantage

At some point, the market will stop falling. It will level off as society moves back to its normal ways in the future, and the market will have a chance to start growing again. This Bear market should be seen as a golden opportunity for us a few years away from retirement. The inflated prices have come crashing down and have now been made more affordable for us future investors. We now have a chance to get in on the bottom as the nation’s economy rebuilds.

How to invest during a crash?

Stay the course on whatever investment plan you have currently been using. For me, it’s a great time for index funds. relatively low risk and always go up in the long term. I just bought another batch with my last paycheck. And with the cheap prices I was able to afford more than I have purchased in a long time. Here at Teachers Stacking 10s, we are a big fan of Vanguard’s system. No particular reason why we just think it is easy to navigate. I have been purchasing more low cost index funds(<.04% fees) during our quarantined time here. There are other stocks out there that can be good buys. There is just more uncertainty with those in these current times. In general, I suggest index funds or something that pays a high dividend. But that's a conversation for a different time. BUY INDEX FUNDS!

What to do during the crash?

Many teachers around the nation now have some extra free time that we aren’t used to. Use it to “Sharpen the Axe”. Now is a great time for reading, research, studying all things finance related, things that you never had time for. Use this time to read a personal finance book. We can recommend a lot of them! Check out the rest of this website plus our other favorites that you can find on our home screen. Take this time to go through your family budget and what your goals are for the future. We have a unique opportunity here to come out of the quarantine as more intelligent investors. Let’s use this time to our advantage.

All finance related inquiries a side. I truly hope this post find you well. We are living in weird times and I believe the nation is realizing how important that role of a teacher is. It’s a great time for all of us to step up and do what we can in our districts to continue to prove our value to society. Thanks for all that you do and spending time to read through our financial advice. Feel free to comment below with any questions or concerns you have during these strange times.

As always…

KEEP STACKIN!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

Minnesota TRA Pension Calculator (High-5 Formula Explained + Examples)

Most Minnesota teachers know they will receive a TRA pension through the

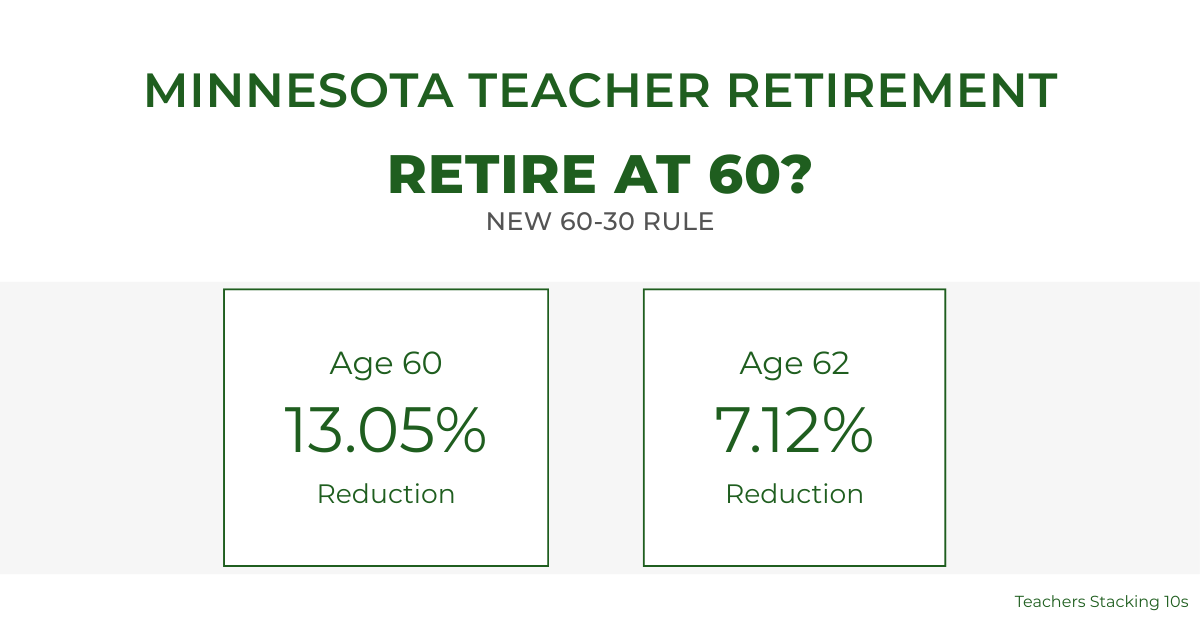

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for