We have talked at length about dividends in the investing world. What we haven’t mentioned is how we use dividends to grow our net worth exponentially through the art of dividend stacking. Dividend Stacking, much like our namesake of Teachers Stacking Tens, is a slow and patient investment strategy that starts with small quarterly and annual growth, and can balloon out to a substantial source of passive income. Like the name suggests, it is not a get rich quick scheme (Those don’t really exist). We aren’t over here trying to time the market buying low and selling high or anticipating the next crash. We are here, buying stable long term dividend growth stocks to increase our net worth.

How does dividend stacking work?

Enter the DRIP – The Dividend ReInvesting Plan. Rather than have those small amounts added into our accounts we have them selected to get REINVESTED back into the company. So each time a particular stock pays a dividend, I am automatically using that money to buy more shares of that company. This embodies that Teachers Stacking Tens philosophy, constantly adding those dividend earning back into more stock which will, in turn, produce more dividends in which you will buy even more stock which will produce even more dividends! You get the idea.

So how do I do this?

Well, chances are your financial institution might be doing this for you already. When you are looking at your 403b or Roth IRA or 401K those accounts will have the dividends automatically reinvested… Nothing you have to do or worry about. For example, in the last 3 years my Roth IRA account has generated $950 in dividends. Those dividends in turn have purchased 3.558 shares of VFIAX. As of Today, that is worth $1,196. So in the last 3 years not only have I used those dividends to purchase more index funds, the value of those index funds have gone up as well. And to be honest I don’t have all that much money in my Roth IRA. Thanks to my need to continue to pay off my new car I haven’t been able to max out my Roth IRA like I would prefer. However, you can still see by being patient and letting our money work for us it has the power to grow exponentially.

So what are we doing with this now?

Like I said, this is something you shouldn’t have to worry about in your retirement accounts. You shouldn’t have the option to cash out your dividends because, you know, taxes… Where this needs to be applied is in your taxable or brokerage account.

Brokerage accounts are a subject that we haven’t discussed in great detail on here for a few reasons. One, there are many financial needs that one needs to understand before getting a brokerage account and two. Brokerage accounts have only recently been redone to be more user friendly. Up until just a few years ago many institutions had a trading fee. Something like $7 a trade seemed to be pretty typical. It didn’t make as much sense to invest small amounts if you were going to get hit with a $7 fee every time. Now many institutions, such a Vanguard, have waived trading fees. There is no fee to purchase most domestic stocks. And many places now don’t have a minimum purchase requirement either. Just that you order in complete shares, and even that rule is changing. More on our Brokerage account set-ups at a later date.

What this has enabled us to do is invest in the market and take advantage of its growth in an account that we can access before retirement age. The Professor is in the second half of his career and is seeing the end in sight (Even if its a long ways down the road). I however am still in the first 1/3rd of my career, retirement benefits 30 years from now are not as clear as benefits that are only 15 years away. I have seen the benefits of investing in an account that I can access should I chose to leave teaching before the typical retirement age. Even though it is taxed, I enjoy this sense of freedom.

It also lets me pick individual stocks not just Vanguard funds. WARNING! – Do not start purchasing individual stocks unless you know what you are doing! This is what we call a pro-gamer move. We’ll have more info to come as we are getting data back from a year of investing in dividend growth stocks. But the short hand is it lets me pick individual companies, collect their dividends, and reinvest them into that company. After a year of experience, I’ve enjoyed it and thanks to dividend stacking, I have some decent returns to show for it and future growth ahead.

– KEEP STACKING!

Minnesota TRA Full Retirement Age: What Age 65 Really Means

Most Minnesota teachers hear terms like Rule of 90 or 60/30 long

Minnesota TRA Early Retirement Reduction Explained

Teaching in Minnesota has become more demanding in recent years. Expectations are

Minnesota TRA Tier I vs Tier II Explained

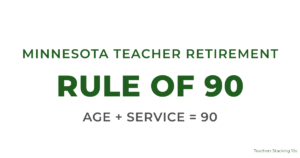

Minnesota Rule of 90: Complete Guide for TRA Tier I Teachers

Minnesota’s Rule of 90 is one of the most consequential retirement provisions

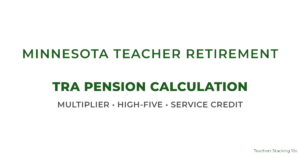

How the Minnesota TRA Pension Is Calculated (Formula, High-5, and Real Examples)

Most Minnesota teachers know they will receive a TRA pension through the

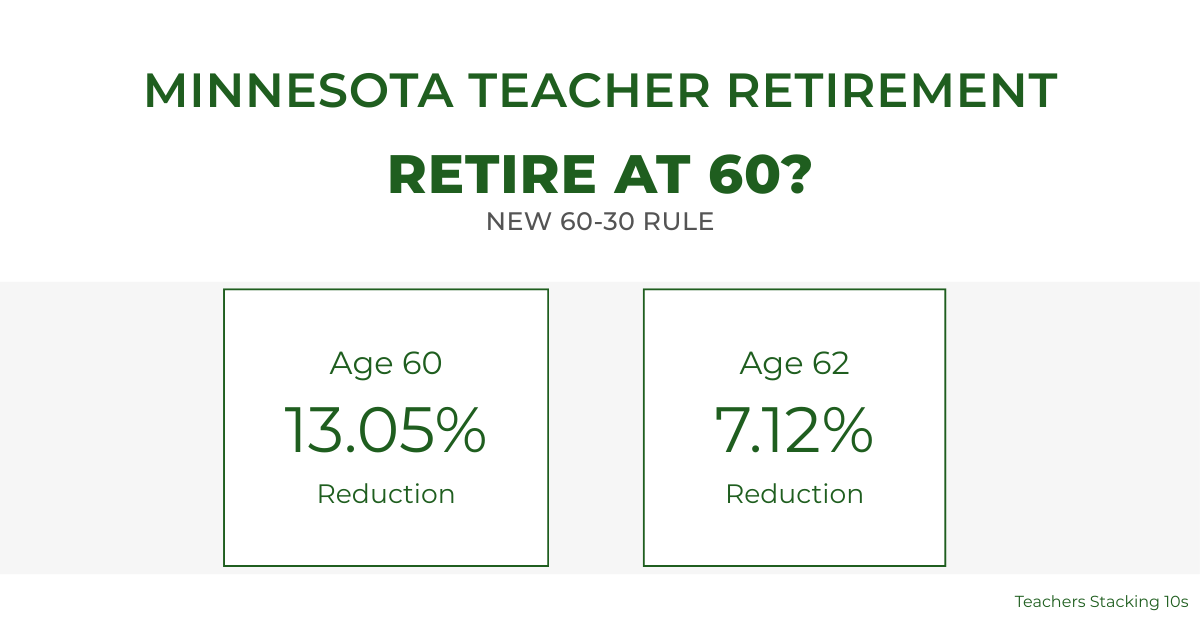

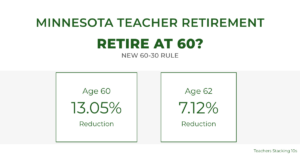

Minnesota Teacher Retirement at 60: Understanding the Enhanced 60/30 Rule

For years, Minnesota teacher retirement at age 60 was financially unrealistic for

.svg")