Well, you wouldn’t think that we would need to put out a post like this since we are dealing with teachers that are supposedly responsible people, but….. People! Check your pay stubs EVERY time you get paid and check on your accounts at least once per month!

If you have followed our advice, much of your paycheck is automatically sent to the proper accounts. Everything “should” be correct and getting to the right places. I mean, those are adults working in the business office, aren’t they? They are, but they are also human, so sometimes mistakes do happen.

The T.A. and I have been dealing with some major issues in our district regarding our paychecks. We are a small district, so our business office consists of one person. Unfortunately, our business manager took a different job in October. Our district hired an agency to handle the finances until the new business manager was hired. Let’s just say that things haven’t transitioned very well. Pay amounts were wrong for certain extra-curricular activities, insurance premiums were not deducted, and 403b, HSA, and other various monies were never sent to the proper accounts. At first, we thought it was just due to the transition. It was, but it happened a second pay period and then even into a third! The T.A. and I contacted our superintendent after the first pay period. By the second pay period, we were bugged, but we stayed understanding. I mean, nobody wins if we go in guns blazing, but we had to make sure the right people were aware of what was going on.

The part that really opened our eyes was that many of our colleagues had no idea that their money wasn’t getting into their accounts! As long as the money in their checking account made it, they didn’t seem to mind that the rest didn’t make it! We talked and encouraged them to check their accounts and make sure that their money was there and accurate. It wasn’t until we informed them that their insurance premiums might not have been paid that they REALLY perked up. It was as if their 403b money didn’t matter. UGH!!!

Now, there was no nefarious activity behind our problems. There was nobody misusing funds or sending them to the wrong place. Apparently codes and passwords needed to be updated with the new company we had hired, but if nobody would have pointed it out, that money might still not be in our accounts earning interest and dividends. Even worse, people might have lapsed on their insurance!

Teachers, we can do better! We have to pay attention to and care about our money. Nobody else is going to care about it for us. If they do, they are trying to get their hands on it!

How the latest from the entertainment giant has me questioning how many streaming services are too many?

Tuesday marked the release of the latest streaming service, Disney+. Disney became just the latest entertainment company to release a service emulated after Netflix’s staple model. Being a huge Star Wars and Marvel nerd I found that trying out Disney+ was a must for me and.. HOLY COW IT IS NEAT! I spent the first hour perusing all of the titles available. After the trip down memory lane perusing old titles that I had completely forgotten about or didn’t know Disney owned, I settled into the

After cranking out the first episode of The Mandalorian, I started to think about exactly how many streaming services I currently pay for each month. I have always considered myself frugal when it came to my entertainment needs. Long ago I cut the cord from cable and relied solely on Netflix and Youtube, undoubtedly a cheaper alternative. But as the years have passed and I have continued to add streaming services to my monthly bill it has come time to question exactly how many do I need and what am I willing to spend each month for my at home evening entertainment. THIS CALLS FOR A SPREADSHEET!

A Look at the 2019 Streaming Services

Here’s a quick side by side look at today’s most popular streaming services available to purchase. Many of these are viewed as alternatives to cable. Each have their pros and cons.

So as you can see, having all the world’s content and your fingertips is far from free. But where do you draw the line?

Take a look at all of those available options above. It’s important to prioritize what streaming services serve you best. At an additional $100 per month for the basic level subscriptions to these streaming services it would almost be cheaper to get a basic cable plan. These pricing also have a way in creeping up from year to year increasing your annual expenses. And this does not take into consideration the opportunity cost of these monthly plans. Setting aside that money in the proper index funds means it is growing at 6-7% and generating dividends. So in reality, spending $1,000 per year on streaming services adds up. I enjoy Netflix as much as the next person but I’ve had that account for 8 years now, that’s roughly $1,200 I’ve paid for one streaming service!

Personally I don’t seem myself getting rid of every single streaming service I am currently subscribed to. But the addition of Disney+ does make me stop and consider what I want to purchase moving forward. One way I’ve been able to keep cost down is sharing the service and pricing with other family members. Cutting your costs in half or in a third makes it easier to justify the spending. Still it’s important to curb some of that spending. Do I really want to pay $15 a month for HBO now that game of thrones is over? Is watching march madness really worth the $6 a month for CBS all access. These are the frugality questions that we should be asking ourselves in all aspects in our lives not just entertainment.

Ultimately you need to decide what brings you joy and what that amount of joy is worth to you. I’ll definitely be keeping Disney+ for the year but might reconsider in the future. Remember when deciding what to pay each month you are taking away from the pot of money that you could be saving for investments or for other aspects of life that bring you joy. For me paying hundreds per year to stream certain TV shows at night might just not be worth it.

The choice is yours, prioritize your spending and as always

The T.A. and I were talking the other day about the fact that we have talked a lot about what to do once you have money, but many people live paycheck to paycheck. It’s time we talk about the biggest problem facing Americans today…. Debt….

One of the first posts that I read when I started down this path was the classic Mr. Money Mustache post on debt being an emergency. I highly suggest reading that post as Mr. Money has a way with words that I still am learning. He is the man!

When it comes to debt, Americans are in love! According to a 2018 study by Nerdwallet, the average American household has $6,829 of revolving balances each month. Add in your monthly mortgage/rent, car payment, student loan payment, etc… It’s no wonder that your average American looks at you like you have a third arm when you ask them how much they are saving each month for retirement.

If debt is so bad, then why do so many people put themselves in this situation? Most people don’t venture out to bury themselves with debt. It’s more like a death through a thousand paper cuts type of situation. They get that first job and see how much money they are going to be making. They decide to purchase a house to start their family. So starts their life of mortgage payments. They realize they need a new/newer vehicle because they “deserve” it. So they take out a vehicle loan with a monthly payment they can afford. They pick up a few things to go into their house to make it look nicer. They go out to eat a few times a month. All of these small charges go on their credit card because they will have enough money at the end of the month when they get paid. Uh oh, the water heater goes out. $1,200. Damn house. They pay that bill because they have to have hot water, but that means they don’t have enough to pay that $500 credit card bill. It’s ok they think because the minimum payment is only $25. They make that minimum payment and carry over that $475 plus another $15 for a total of $490. Here’s where it all starts to go wrong. They don’t change their habits. They rack up another $500 in credit card charges the next month and now have a $990 bill staring them down. Get the picture?!?

So how do we handle this debt problem? Well, if you’re like most Americans, you ignore it and try not to think about it. You DEFINITELY don’t talk about it. The typical American sticks their head in the sand and hopes the debt will go away. THAT WON’T WORK! So what do they do? They run out and get a consolidation loan or even a home equity loan and pay all them cards off! Problem solved! Wrong. Wrong.

Because here’s what happens. All of their debt is gone, but their habits don’t change. They continue to put those little charges on their credit cards and now, not only do they have that new loan payment, but their credit card debt starts to climb again. It’s an all-too common theme in America. People NOT taking responsibility.

So professor, what’s the answer then? How do I fix this situation?

First, you must face up to your debt and NOTignore it! Immediately stop spending money on those credit cards. Put every penny you can spare into paying them off. You can start on the card with the smallest balance or the highest interest rate. Hard-core budgeters will tell you it has to be the highest interest rate card, but you need to do whatever works for you! It won’t be easy. It will probably suck, but YOU put yourself into this situation and only YOU can get yourself out.

For many of us, car shopping is one of the great frustrations in life. You spend weeks if not months researching and searching for options only to either spend too much money or end up with something that is unreliable. The finance community has all kinds of feelings and opinions on purchasing vehicles. I don’t know that there is a one size fits all model for your car shopping experience, but there are definitely some bad car-buying decisions that can be made. The following is a walk-through of my decision-making process resulting in my ultimate purchase of a (gasp) brand new vehicle.

Much of the F.I. community would be appalled at my decision to buy a brand new vehicle. For the typical person, it might not have been the best decision to fit their lifestyle but after my debate and research, I do feel that it was the best decision that fits my lifestyle.

The old reliable Toyota Camry

Transportation Priorities

Fuel-Efficient

Reliable

Storage Space

Okay for winter conditions

Longevity

Fuel Efficiency – My number 1 priority for a vehicle is its fuel efficiency. I want to be as environmentally conscious as I can as well as saving money on the monthly gas bill. I commute 70 miles a day and travel a lot in the summer and on weekends. Having a gas guzzler just doesn’t make sense to me. This rules out any kind of truck and really anything with 6 cylinders in general. My target while searching was 30 MPG.

Reliability – I need my vehicle on a daily basis and I don’t have a realistic backup. Additionally, I have very little knowledge when it comes to mechanical workings under the hood. I can do the basic maintenance myself. After that to fix something I would need a solid youtube tutorial plus a lot of free time, which is something I don’t have during the school year. I am envious of those of you with that skill and are able to drive around ridiculously old cars that are cheap because you have the skill set to keep them functioning. However, I do not currently have that ability so this essentially ruled out any of those ultra-cheap and old cars.

Storage Space – I have spent the last decade of my life driving the hand-me-down family sedan. I made the decision that I would like to have some more potential for storage space. Once again I spend my summers travelling in my vehicle. It would be nice to not have to fill it up to the brim ever road trip I take. Likewise, I enjoy my outdoors activity so a more accesible backend is what I was looking for. Essentially this narrowed the search to vehicles with a hatchback.

Snowy Conditions – Living in the North does bring about its limitations. Like I said I drove the family sedan fine in the winter for a decade. However, I had to always be conscious about snowfall and storms and it is nerve-wracking driving a 2-wheel drive vehicle on snowpacked roads. Had I ever had an accident? No. Was I ever stressed driving? Yes. So for this, I was really hoping to get something that had 4 wheel drive. It was my last priority but it was definitely on my wish list. It also made me hesitant to buy an electric vehicle. Last year we had several days below the -20 degree mark and I park outside. Current battery technology is astounding but I did not have faith of that battery holding up the same 10 years from now.

Longevity – I am not a car guy. I don’t like constantly searching for cars. Hence my being okay driving a hand-me-down Camry for 10 years. In my search I was hoping to find something that I could get several years out of. I put over 20,000 miles a year on my vehicles and I wanted something that I could drive for at least 5 years. In my mind this ruled out many vehicles that were well over that 100,000 mile mark. Yes there are brands with great reputations for running well beyond 200,000 miles but there are also brands that have the habit of wearing down and starting to be problematic once they get over 150,000.

Before all of the hardcore frugality types start tearing some things apart I would like to make it clear that up until this point I reached 270,000 miles on my slowly decaying toyota camry. It’s missing 2 door handles, the AC only works on certain settings and it doesn’t like that cold weather. I’ve reached the point where I have lost confidence in being able to drive it across the country in the summertime. Also, For the extremist out there thinking that why am I wasting my time driving to work rather than get a closer job and bike or walk for a commute saving thousands I will say you are correct but that isn’t what fits my lifestyle right now. I enjoy the place that I work at and I enjoy the city I live in. To me, that is worth the extra money every month.

And the winner is…

The 2018 Subaru Forester. Cheaper than the CRV Rav 4 with similar fuel efficiency and reliability. More reliable and better-predicted longevity than the Ford or Chevy equivalent.

The reason I ultimately chose the newer vehicle boiled down to 2 things. The Vehicle had 0 miles on it and was under warranty for the first 60,000. and I was able to get 0% financing. To me this was big. 0% financing meant that I would pay ZERO INTEREST for my car. At that point, I decided that I would get a new car. The only thing to decide was how much I wanted to put down.

I determined the amount I could put down based on how much I could pay each month. I felt comfortable with a $500 monthly payment for 4 years. To achieve this I put $4,500 down. Technically I would have been better off putting that into an account to gain interest but that’s not how my habits work. I was better off putting that money down on the car and keeping that $500 a month car payment.

HOW ON EARTH DID I JUSTIFY BUYING A NEW CAR? It’s a terrible investment right? depreciates as soon as you leave the lot. All of this is correct. I justify the brand new purchase with the idea of how I drive cars. My plan is that I won’t be looking for a new car again until the 2030’s. If I can get 12 years out of the vehicle, all of a sudden that $500 a month payments turns into $165 a month. Much more reasonable and definitely something to consider when car shopping. To me it’s worth the bad investment to not have to worry about my daily ride to and from work. Ultimately I would like to have a much shorter commute, allowing for me to have a cheaper car that barely gets driven but for today that’s not what is most practical.

A year later…

Well, it’s been a year since I bought the Subaru Forester and I have to say I enjoy it a lot. Some things that I have noticed…

I put a lot of miles on vehicles…

4 wheel drive is a nice perk but it doesn’t mean you don’t have to be careful driving in ice and snow.

Cars made in 2018 definitely ride differently than cars made in 2001.

Extra cargo space has made traveling more convenient and less stressful.

I’m averaging 33.0 miles per gallon since purchasing the vehicle.

losing out at $500 a month that I could be investing hurts. But it is manageable knowing that it is a temporary cost.

So overall a positive buying experience. And like I said, while it as not been fun paying $500 a month for a car payment I know now that I can do it and still have enough left over to invest. Meaning once I pay off the vehicle that will free up another $500 a month to invest.

I think buying a new car was the right choice for me at the time. It could also be the right choice for you or maybe it’s not. When buying try to take your own bias out of it and create a checklist of your priorities, just like I did. Then see what types of car fits your needs the best. Until then,

KEEP STACKIN!

I feel less like an idiot now seeing JL Collin’s post!

Some people love to travel the world and see different things. I am not one of those people. I am very much a homebody, but as I get older, I am realizing how much I hate the cold winter weather and want to head somewhere warm. This year I decided that my wife and I are going on a vacation. After looking at our budget, I realized that we would have to blow it up to make a nice vacation work. I knew I would have to find a way to pay for it that was “unconventional”. Hello, travel rewards credit cards!

If you’ve been reading this blog, you remember my post on the cash-back Discover It card. After that successful venture, I started doing more research into using credit cards for the travel rewards. I ended up choosing the Chase Sapphire Preferred card for it’s excellent bonus. After spending $4,000 in the first 4 months, I would be eligible to receive 60,000 bonus points. This was easy enough as I had been paying our monthly bills on the Discover It card for the previous year. I just changed those payments over to the Chase Sapphire Preferred card. We easily met that minimum spend in the first 3 months, and BOOM, 60,000 bonus points were added to our account. At that point, I started paying our monthly payments on our Chase Freedom Unlimited card because we earn 1.5 pts for every dollar we spend. Then I transfer those points to my Chase Sapphire Preferred card because those points are worth 1.25 cents/point when redeemed for travel through the Chase portal! Double-hacking!!

An added bonus was you can get 15,000 point for every friend you refer that qualifies for a card. So being the great friend that I am, I referred the T.A. Once he qualified, another 15,000 points were added to my card. I’m such a nice guy!

So after paying our monthly bills over the last 8 months on the Chase cards, we ended up with over 94,000 points!

Monthly spending points – 19,512

Referral – 15,000

Bonus Points – 60,000

Total points – 94,512

After accumulating these points, we decided that we wanted to go to Cabo. We are lucky in the fact that my parents have a timeshare, and we were able to get a FREE 6 night stay at a resort there through my parents’ point portal. I looked into flights and was able to get round-trip flights to Cabo for 91,163 points! FREE FLIGHT!

The Professor taking it all in.

Granted, the die-hard travel hackers out there could have done this more efficiently and for better “value”, but for my first time, I’m pretty happy with the results! Another example of making the credit card companies work for you! And hey if you decide you’d like to try the Chase Sapphire Preferred card. Here’s a referral link that you can use.

“Be careful on what size of house you buy because you’ll end up buying enough crap to fill it” – Papa T.A.

In the fall of 2015 I purchased my first house. I had been bouncing around to different apartments and rental houses for the previous 7 years, all the while paying someone else to live in their place while they generated some nice passive income from me. Finally, I decided enough was enough and purchased my first home. A small, 2 – bedroom house that was over 100 years old and in need of several cans of fresh paint. As I was looking at houses I remember my father, a life-long frugal man, comment, “Be careful on what size of house you buy, because you’ll end up buying enough crap to fill it.” Being in my 20’s and used to the annual purge that comes from switching apartments I thought there was no way I would ever fill an entire garage, 2 bedrooms, a basement and all of the storage that came with it. Fast forward to 2019 and low and behold I have managed to fill my small 2 bedroom house with crap.

While many human beings do this same thing with their own homes I think it is far more dramatic with our Paychecks. Think back to a time when you first started working. Go look at those old paystubs and see what you were able to live off of when you first took that teaching job. How many started below $40k annually? How many below $30k? Yikes. Yet we, for the most part, were able to pay bills, enjoy life, take vacations etc. on that smaller amount of money. in 2019, I make considerably more than I did in 2012, On average $500 a check more, Yet I still find myself feeling financially stressed at times. How is this possible? Making $1,000 more per month yet still have financial stress? The answer is Lifestyle Inflation.

Spending that bonus check before you’ve seen it!

Lifestyle Inflation is when our monthly expenses slowly creep up to match our added income. Sometimes it shows up as an immediate purchase shortly after or even before an expected raise or bonus comes in. Think, Clark W. Griswold spending his Christmas bonus on a swimming pool before even seeing if he got an bonus or not. Other times it creeps up on you in small extra expenses that consistently add up. For myself, this manifests in craft beers and Amazon purchases. 22-year-old me had no problem walking past the local 6-packs to grab the Buschlight for a fraction of the price, He also would’ve laughed at me for being an amazon prime member because why on Earth would I be buying that many things online, there wasn’t any more room in the apartment! Small expenses like this continue to add up until you hit that stress point again and you’re right back to where you started financially; stressed, not saving anything, and assuring yourself that if you just made more money that would be the answer. Well, I have news for you, if you don’t confront the lifestyle creep no amount of income will ever be enough. Case in point – Had a conversation with a friend of mine who is in the private sector. Making well over what a teacher would make. He is fixed on the idea that once he gets his next bonus then he’ll really be able to start paying down his student loans and truly investing. He says that as he makes $80k a year. However, his rent is triple what my mortgage is, he likes his new cars and nice watches etc. So simply getting more money for most of us won’t save us from that financial stress. You need to FIGHT THE LIFESTYLE CREEP!

So how can we fight this? Auto investing is a great first step. Schedule a transfer to your savings account or your investment account shortly after your payday. For me, it’s the next day. So many time I don’t even see the full amount of that paycheck in my account before a couple of hundred dollars are pulled out and put into an account that I won’t spend down. Another great way is to up your increase to your 403b. This is a pre-tax contribution so there are some additional benefits for choosing this route. It is harder to access this money in a pinch so I tend to only increase my 403 contributions slightly each year. Similarly, you can increase your contributions to your HSA account. Basically, save first, not last. If you choose to look at your account at the end of each month and save whatever is left it’ll always be less than if you were to set an amount to get taken out of to start with. In addition to saving first, you should just be aware of that inflation creeping into your life. As you are online shopping or getting your groceries for the week don’t forget about your frugality just because you got paid yesterday. Evaluate your financial decisions based on the happiness those purchases will provide you. Don’t buy a $250k house just because that’s what your friend did, think about what will make you happy. A big house with a big mortgage payment with all kinds of rooms to start accumulating your own collection of crap. Or a smaller house with a smaller mortgage payment and some money to invest or to travel or to do whatever it is that brings you joy.

So take some time and look back at those early checks to see what you used to be able to live off of. Figure out how much you want to start auto-saving even if it’s $50 just start. Lastly, look at what you are buying and how much joy that purchase is bringing you and decide for yourself if it is worth it or not.

So how can someone who is an average wage earner grow their money like a rich person? The answer lies in… math!

We’ve all heard stories about how some little, old lady with no family and worked as a librarian all her life passes away and leaves behind a $2,000,000 estate! People far and wide wonder how could this woman who earned at most $35k in a year could accumulate that much money! The reason is the power of compound interest!

Compounding Interest

Interest is the money you earn from financial institutions for allowing them to use your money to loan out to their clients. Banks can pay you this interest because they charge higher interest rates to their clients. So what is “compounding interest”? Compounding interest is how your money grows each year. Look at the following example.

Let’s say you deposit $10,000 into a savings account that will pay you 2% interest each year. This is a very realistic rate that you would earn from a savings account from an online banking institution. What’s not realistic is we are not going to be adding anymore deposits to this account during the year. At the end of the first year, the bank adds your 2% in interest to your account. Again, they will usually do this monthly or quarterly, but we are going to keep it simply with yearly interest. So they add $200 to your account. Now you have $10,200 in your account. At the end of the second year, they add another 2% in interest, not just on the $10,000, but on the $10,200 that you now have. So at the end of the 2nd year, they add $204 to your account. Now you have $10,404 in your account. End of the 3rd year, they add another $208.08 giving you $10,612.08. That is compounding interest. This might not seem like great growth, but that’s the process. The better return you can get from your money, the faster it will grow.

The Rule of 72

We’ve looked at compounding interest. There is a simple way of calculating what your money will do over time. You look at your rate of return and see how many times it will go into 72. The total will be how many years it will take you to double your money. So in our previous example of 2% interest, we would double our money every 26 years. Not a great rate of return. Let’s say we take that same $10,000 and invest in the stock market that will return on average 7%. We should double our money in 10 years. Everything rounded to the nearest whole dollar.

Starting money – $10,000

Rate of Return 7%

Year 1 – $10,700

Year 2 – $11,449

Year 3 – $12,250

Year 4 – $13,108

Year 5 – $14,026

Year 6 – $15,007

Year 7 – $16,058

Year 8 – $17,182

Year 9 – $18,385

Year 10 – $19,671

So you can see that after 10 years, even with you doing absolutely NOTHING, you have doubled your money! This is without you adding ANY more money into your account! This is the power of compounding interest!

Now let’s look at an that same scenario except that we will continue to add $100/month to that account since we should constantly keep saving.

Starting Money – $10,000 adding $100/month

Rate of Return 7%

Year 1 – $11,900

Year 2 -$13,933

Year 3 – $16,108

Year 4 – $18,436

Year 5 – $20,926

Year 6 – $23,591

Year 7 – $26,443

Year 8 – $29,494

Year 9 – $32,758

Year 10 – $36,251

So just by adding another $100/month into our account, we have increased our total savings by another $16,500. This is something that you can achieve! Now let’s imagine you have followed the T.A.’s advice and have become a super saver $500/month. What would those numbers look like?

Starting Money – $10,000 adding $500/month

Rate of Return 7%

Year 1 – $16,700

Year 2 – $23,869

Year 3 – $31,540

Year 4 – $39,748

Year 5 – $48,530

Year 6 – $57,927

Year 7 – $67,982

Year 8 – $78,741

Year 9 – $90,253

Year 10 – $102,570

This is where you can really start to see why we need to work on that savings rate and how we can start to build true wealth. So as you continue to build your portfolio, you can start to project the money you will have as you go through the years.

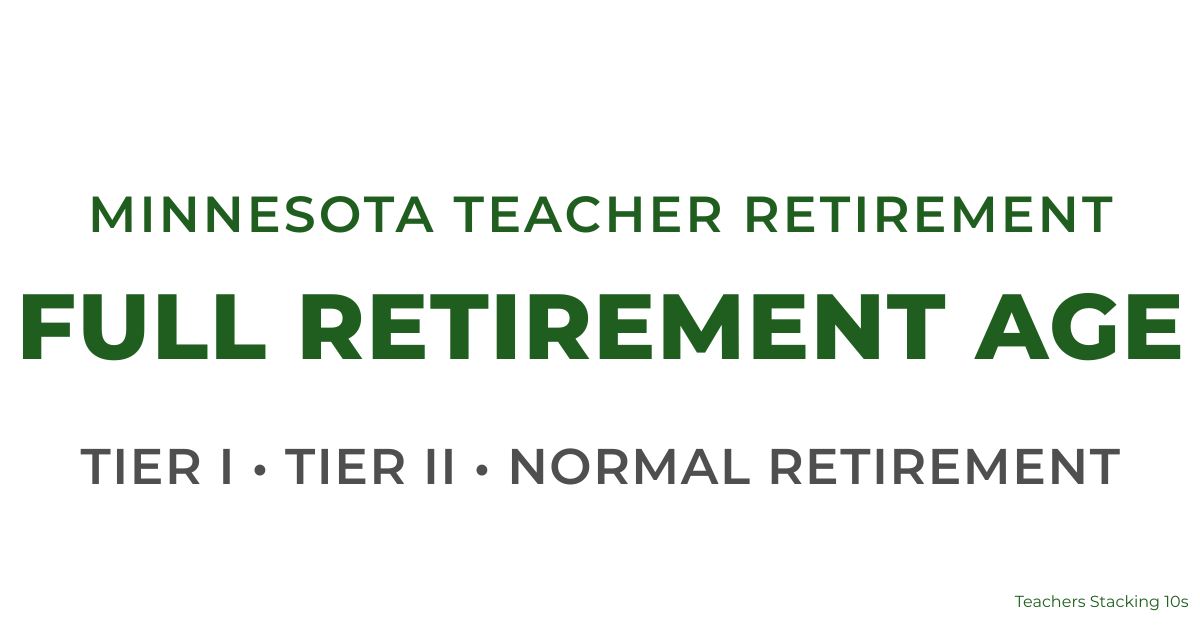

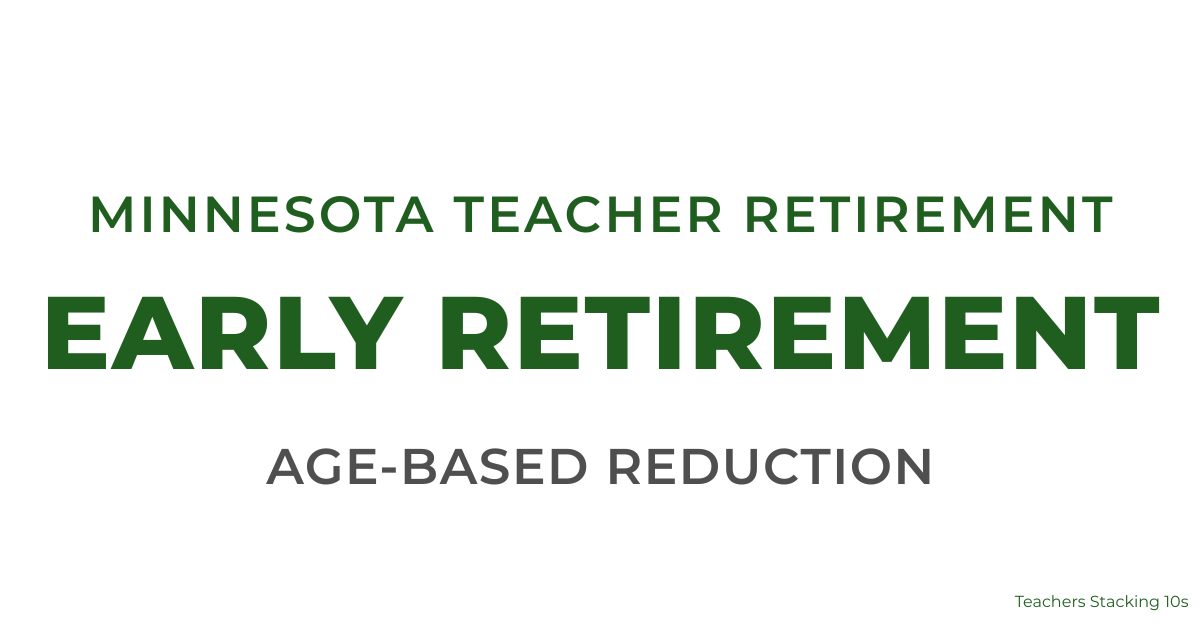

Minnesota TRA full retirement age is 65. Learn what normal retirement age means, when benefits are unreduced, and how early retirement reductions apply.

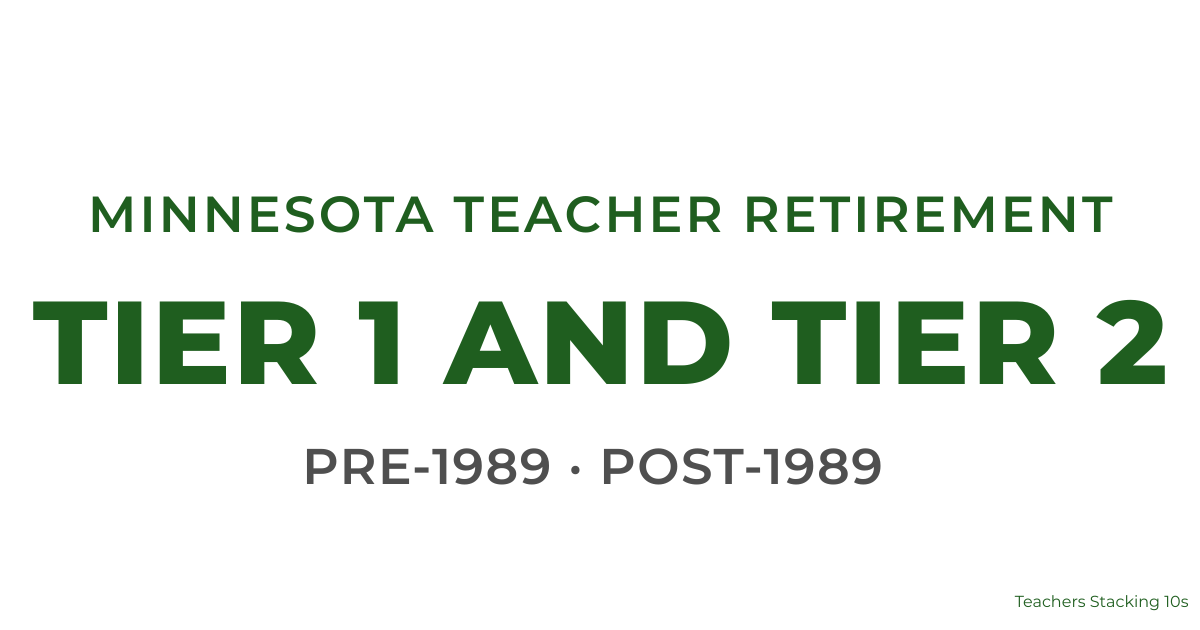

Minnesota TRA Tier I vs Tier II is based on your hire date and determines whether you qualify for the Rule of 90, what your full retirement age is, and how early retirement reductions apply. Understanding your tier is the first step in building an accurate Minnesota teacher retirement plan.

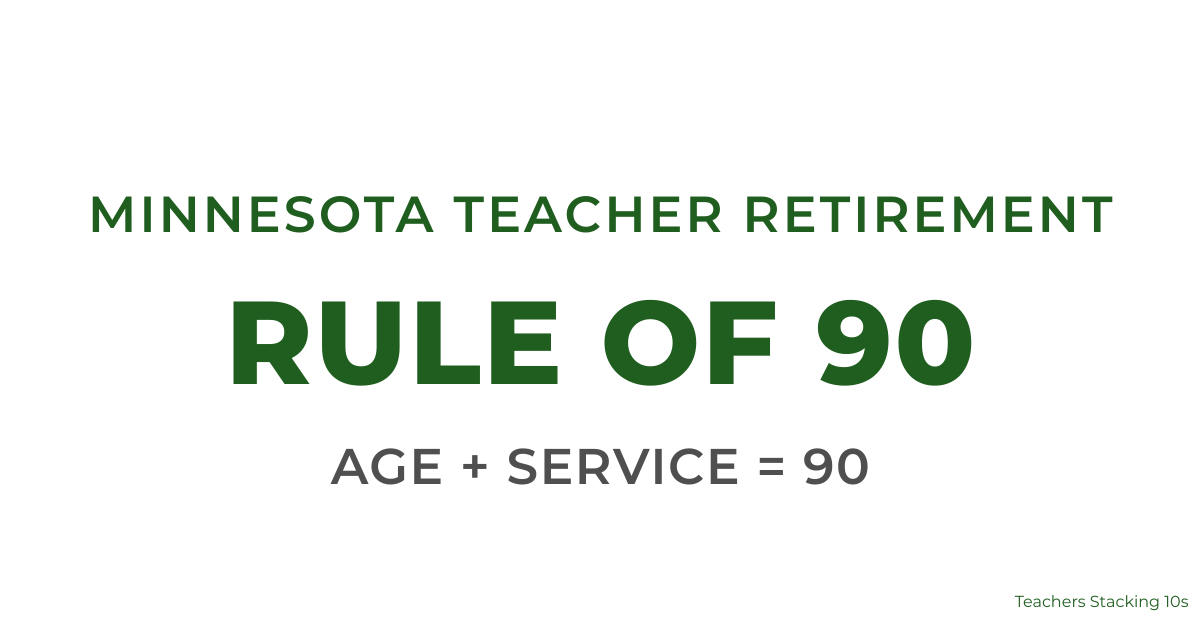

Minnesota’s Rule of 90 allows certain Tier I teachers to retire when age plus service equals 90 without early reduction penalties. Here’s who qualifies and how it compares to 60/30.

A clear breakdown of how the Minnesota TRA pension is calculated. Learn how multipliers, High-5 salary, and service credit determine your benefit, with real examples and early retirement comparisons.

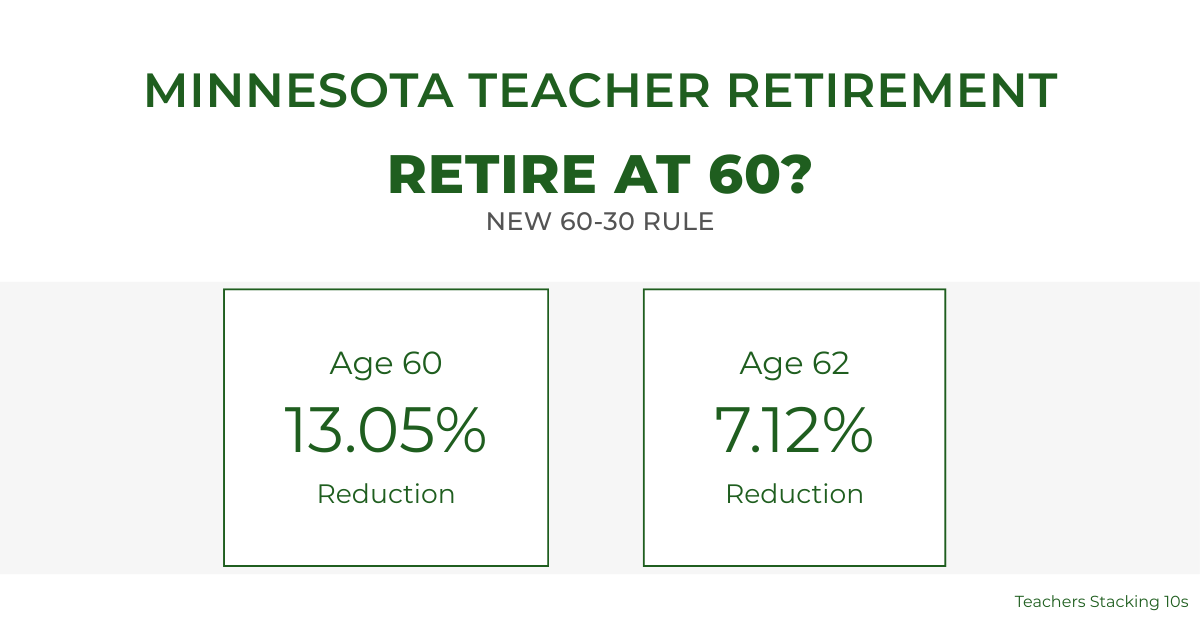

Minnesota’s new 60-30 pension rule is a historic win for educators—allowing earlier retirement with fewer penalties. It brings long-overdue fairness to Tier 2 teachers, boosts retention, and signals progress. But the fight isn’t over—educators must still push for an unreduced 60/30 career rule to achieve full equity and security.

We’ve spent a lot of time talking about investing, but you might be saying, “Professor, I’m living paycheck to paycheck. How do I find any money to invest?” This is a great point. I was in the same position 2 years ago. I lived the paycheck to paycheck lifestyle. I didn’t think it was too bad, but I knew there had to be a better way.

I did some research into how to increase your free income. Most of the sites I found made it seem to easy! You just walk into your boss’s office and ask for a $25,000 pay increase. I actually found that advice. Well, it was a little more technical than that. You proved your value to the company, found a competitor that paid more, and then discussed the increase with your boss. Imagine doing that as a teacher. You find another district that pays $5,000 more per year than your current district. You walk in to your superintendent’s office and say, “I have accomplished great scores on our yearly assessments, and I know that I can make $5,000 more per year at district X. I’d like you to match that pay or I will leave.” Undoubtedly, your superintendent will thank you for your service and wish you luck at your new job. As a teacher, we don’t have some of the luxuries that the private sector does when it comes to salary negotiation. Of course in other posts, we have also pointed out some of the advantages we have over the private sector.

So we could look for ways to increase our income outside of teaching through the use of side hustles or summer jobs, but in this post, we are going to look at the other side of the equation. So what areas can we cut our costs?

Housing – When we look at where we can cut costs, we want to start with the biggest areas first because they will have the biggest impact. Housing is most people’s biggest expense each month. It can also be difficult to change due to family situations. If you are able, you could look into smaller houses or apartments to lower your rent or mortgage. You could also look into renting out a room on your property if you are comfortable with that. This would be a great option for a younger teacher that could rent to another teacher in their district. We were not able to change our housing expense at all. With a wife and two teenage girls, we were definitely not comfortable renting out a room in our house. The TA, on the other hand, was able to rent out a room to one of his friends. This is a great financial move for him!

Cable/Internet – This is another area that can be a huge expense each month. Before our cost cutting moves, we were paying $150/month to Dish Network for our cable alone. I looked at our list of channels and cut our bill down to $100/month! I then called last month to say that I felt we were still paying a little too much and they lowered our bill down to $70/month for being a loyal customer. This is something that everyone can do. EVERYTHING is negotiable! Companies spent incredible amounts of money to attract new customers. They claim that those “specials” are only for new customers, but if you call, and calmly discuss the fact that you have been a loyal customer for many years, they will pass you along the chain until you reach the customer retention department. They are the ones that have the power to authorize these “special” rates. Ramit Sethi in his book, I Will Teach You to be Rich, has scripts that he uses to help you negotiate lower rates on everything from cable to car insurance. Very useful tools! I know, I know… There are many different options for TV online, such as Netflix, Hulu, etc. We haven’t quite gotten to that point yet. If you live in a large city, you also have a variety of options for your internet service and speed. Living in rural Minnesota, we are stuck with our current ISP. If you have the options, this can be an area to cut a good amount of money.

Groceries/Food/Dining Out– This area can vary drastically from person to person. If you are young and single like the T.A., your grocery bill is probably fairly low, but your dining out bill might be sky high (damn parmesan-garlic wings)! My grocery bill dwarfs his each month, and with two teenage girls, my dining out bill probably isn’t far off of his. Really, the only way to cut this area is to track your spending each month. A tool like YNAB (You Need A Budget) is a great tool to use to track these expenses. A quick way of saving money in this area is to eat at home more often. This can be a very easy change, but many times, change can be difficult. Even with a laser focus, we have had a difficult time trying to cut our costs in this area. It is SOOO convenient to stop at a fast food place or a restaurant instead of eating at home. You actually have to stop, think, and plan your spending!

Cell Phone – This is a huge area of expense for a lot of people. In our family of four, our plan with Verizon was a whopping $250/month. This is a huge kick in the ass for your budget. I looked into it a little bit and noticed we were paying insurance on our phones that were already paid off! I went online to our account and removed that insurance and immediately knocked $25/month off of our bill. Super easy! I have also looked into doing Verizon pre-paid as I’ve heard that it is sometimes up to 50% off your bill. I haven’t been able to take that step. There are also other plans out there likeStraight Talk, Republic Wireless, Google FI, among others. I will not speak directly to these yet since I have not had any experience with them. Once our kids are off our plan, I will definitely look into these other options to cut costs even more!

Insurance – Insurance, or “in case shit happens”, is really a necessary evil. Think about all of the different kinds of insurance that we have. Health, life, auto, home, dental, umbrella, that’s quite a list! Now, not everyone has to carry all that insurance. We won’t cover which of these insurances you should or shouldn’t carry, but we do want to look at how you can cut costs. The first step is to look at how much coverage you have. You could save money by raising your deductible on your health or auto insurance. This will save you some money, but the bigger savings will come from shopping around. The longer you stay with the same insurer, the more they will automatically raise your rates. I learned this firsthand last year when I shopped around for new auto insurance. I had been with the same national agency for my entire driving life (almost 30 years). I knew my agent very well and could talk with him whenever I needed. I sat down with him to see if I could lower my costs. He punched some numbers, but there wasn’t much he could do. The computer just kept spitting back the same premiums. I visited with a couple other insurance agents, and I was shocked at the difference. See the numbers below to how much we saved.

Category

Company A

Company B

Difference

Monthly Premium

$178

$85

$93

Deductible

$500

$500

0

Coverage Amounts

$100k/300k

$250k/$500k

DOUBLE!

I couldn’t believe it. I cut my monthly cost in half AND doubled the amount of coverage I had. I wish I had shopped around for insurance years ago. Think of how many hundreds, if not thousands, of dollars I had lost over the years. It was incredible! Definitely shop around for your insurance. Now, things like healthcare might be tied to your employer, so you might not have the option of shopping around with different carriers, but if you can, DO IT!

There ya go. Five HUGE areas that you can cut a great deal of expenses to allow yourself more money to put to work for you! Don’t tell yourself that it can’t be done! Get out there and try. I didn’t think it was possible either, but it is. You just have to make the effort! Now get to work and…

We all know how busy life gets Once August and September roll around. Do yourself a favor and takes these 5 financial steps now to help automate your finances for the upcoming school year.

1. Set up an automatic deposit into a savings account with a decent interest rate.

At the very least start having money automatically pulled from your checking account into a decent (greater than 1% interest) savings account. I started just by having $50 automatically transfer at the start of each month. It sounds small but pulling that money out of your checking account each month adds up in a hurry. If you are like me, I tend to spend whatever is in my checking account. It is crucial for my savings to have that money come out right away to the point where I basically never see it. I forget the fact that I am saving money first.

2. Check to see that you are getting a real interest rate on your savings account.

Four years ago I, like most people, had a savings account through my local bank. Turns out that savings account was earning a whopping .05% interest… What a waste! Currently I have a capital one 360 account (affiliate link). It’s not extravagant but it earns 1% interest. That is 20x the rate of my local bank! You can find some banks out there that will offer up to 2.5% but as long as you are up over that 1% mark at least your money is doing something while it is sitting in the bank. Personally, I don’t keep a large sum in a savings account. I prefer to have that amount invested, but it is nice to have a little cushion in cash available.

3. Increase your contributions to your investment accounts (403b, HSA, Roth IRA, etc.)

You should have some kind of an investment account that you contribute money to. At the start of each school year, I slightly increase the amounts I contribute to each of those accounts. I like for my increased contributions to match whatever my raise will be for the upcoming year. I have figured out the monthly allowance that I can live very comfortably on ($2,600). At the start of each school year, I will increase my 403b, HSA and Roth contributions so that my take home each month is roughly $2,600. Doing this prevents me from getting the lifestyle inflation that comes from earning more money and beefs up all of my investment accounts.

4. Automate your bill paying

Paying your monthly bills can be time consuming, and if you’re like me, another thing that you can potentially forget. Go through all of your accounts – Internet, Electric, Gas, Trash, Mortgage, Car Payment, Student Loan, etc. and set all of those bills to auto-pay. It might be nerve-wracking at first but in the long term it saves you a lot of time and mental energy to automate all of those bills. Typically, if you go under account settings there will be an option to auto-pay. For me it has freed up time and has reduced the amount of stress in my finances. Knowing that my bill will automatically be withdrawn from my checking account is one less thing I have to worry about during the school year.

5. Establish a preferred way to track your spending

If you aren’t tracking your spending and your net worth, then you aren’t paying attention to the number 1 factor in your journey to your financial freedom. There are a lot of services out there. A lot of great ones are free. I personally use Mint and Personal Capital to track my spending and my net worth. I feel like those do a nice job of tracking all my finances. I like having Mint to track my day to day expenses and I primarily use their monthly spending categories feature. I use Personal Capital to track my net worth. I feel that it does the best job tracking all of my accounts collectively and giving me an accurate look at what my net worth is and is the site that I reference when I set my net worth goals for the year.

After all of that is said and done, I still like to use a spread sheet that helps track spending and net worth over time.

Credit cards… For some people, they are a symbol of debt, despair, and frustration. For others, they are a symbol of income, joy, and motivation. How could a small piece of plastic stir such different emotions in people. For this answer, we need to analyze how people deploy these cards in their lives.

The Good

Let’s start with those people that use credit cards to the benefit of the holder. In recent years, credit cards have worked hard to recruit new card owners by offering some great sign-up bonuses. These various bonuses include; cash-back and match rewards, travel miles, and card points that may be redeemed for gift cards or other redemption portals. Some of these bonuses are one-time hits for meeting certain spending requirements. For example, I just recently met my spending requirement on my Chase Sapphire Preferred card. The spending requirement was $4,000 in the first 3 months of card ownership. By meeting this requirement, I was awarded 60,000 bonus points. (I will do an in-depth case study on this card in a future post.) Others are continuous bonuses that are earned each time you spend money on the cards. My case study on the Discover It card was an example of a cash-back card. These people are go-getters that think about what they want and find a way to make it work for them. Credit cards are a means to an end for them. The most important thing about these people is that they pay their statement balance in full each month. They do NOT pay interest to the credit card companies. That would defeat the purpose of getting those bonuses because the company might pay you a 2% cash-back match for your spending, but they will charge you in excess of 25% interest if you carry that balance forward!

I am one of these people, but I wasn’t always….

The Bad

The next group of people are those that use cards to pay bills, expenses, and other items both necessary and unnecessary. These people do not plan their spending on their cards. They lose out on getting great bonuses. These aren’t bad people. In fact, I used to be one of them, and I’m not half-bad (at least according to my wife). They just need a little guidance and direction. One important thing that this group needs to improve upon is creating and sticking to a budget, as you can see here. This step in the process can be a very difficult one because people at this stage have probably never used a budget before. They have just spent money as they needed it. This is the point where you become proactive instead of reactive with your money. These people end up paying that 25% interest on their cards because they can’t quite afford to pay the full statement balance. They “justify” carrying that balance because the interest might only be $25/month. This is the “monthly payment” mindset that I will touch on more later in this post.

The Ugly

This final group of people are ones that take spending on their credit cards to the extreme. Not only do they pay their bills on their cards, but they also put unneeded expenditures on them. The biggest problem is that this group has one or more maxed out credit cards with not enough cash to pay them off in the next month, or in some cases, in the next few years! They end up paying hundreds, or even THOUSANDS of dollars every year in interest! They are GIVING money to these credit card companies. Credit cards for this group cause fear and anxiety. You can’t talk with these people about credit cards and responsible spending because they become angry and defensive. I’ve tried to have small conversations with some of my closest friends about this, but I’ve learned that it’s not a topic that people are comfortable talking about. I’ve gotten to the point that I don’t even talk about our financial situation with others unless they ask, and even then I just say that we don’t have any credit card debt and if they ask, explain how we were able to accomplish this.

I feel bad for many of the people in this group, and I don’t want to come across as callous, but honestly, it’s usually their own fault. I realize that there are things like medical emergencies that can destroy and families’ financial future, but those are the exceptions and not the norm.

So how did we go from the ugly to the bad to the good???

The Process

The first step for us was to actually realize what we were doing was stopping us from doing the things we dreamed about doing and our retirement goals. I studied our monthly spending and realized that we were losing over $250/month to credit card interest!!! We were so stupid, but the thing is.. we could afford our monthly payments. We weren’t adding anymore to our debt, but we just weren’t really digging our way out. This is true of most Americans. We have been trained to think monthly payments are required. MONTHLY PAYMENTS are bullshit! If you want to gain financial security, you MUST eliminate the term monthly payment from your vocabulary! The only monthly debt payment you should be making is your mortgage.

Once we admitted our problem, we developed a debt payment plan. We chose a debt snowball strategy. This is where you list all of your debts on a piece of paper in order from smallest to largest. We then proceeded to pay the minimum payments to all debts except for the smallest one. We put as much as we could until it was paid off. We then took that “extra” money and added it to our next smallest debt. We did this for 3 years until we had paid off all $18,000 in credit card debt we had. Now, people will tell you that you should pay off the highest interest debt first. This is really the most efficient way of paying your debt, but my wife and I needed the emotional “win” to keep us motivated in paying our debts. If we would have started with our $9,000 credit card, it would have taken us over 20 months to pay it off. This would have been a long time to wait for a “win”. We may have lost our motivation and slipped back into paying the monthly minimum. We’ve all seen those minimum payment graphs on our credit card statements, so I won’t bore you with that, but you MUST find a way to pay more than the minimum each month on at least one card.

At the end of those 3 years, we had reached the top of the mountain, or so we thought. We had eliminated all of our credit card debt. We had moved from the ugly to the bad. How did we move into the good? I had read various websites like Mr. Money Mustache, and realized I wanted those credit cards, who we had paid so much in interest to, to actually pay us! I chose to start with the Discover It card. I was approved for the card and began paying all of our monthly bills on it. Each month, we paid off the card in full. The KEY is that you MUST pay your statement balance in full each month. If you cannot have the discipline to do this, DO NOT attempt to use this strategy. You’ll end up paying more in interest than you will receive in benefits.

Finally, we had turned the tables on those damn credit card companies. For 25 years, all the way back to that Citibank card that I signed up for on Spring Break back in 1993 (but I got a sweet T-shirt!), I had been paying interest. Now the credit card companies pay us. And you can make your credit cards work for you too! Take that ugly situation, analyze what you can do to fix it, and turn it into a win for you. It may take some time and discipline, but you can do it!